studiu comparativ privind sistemele contabile

TRANSCRIPT

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 1/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

133

STUDIU COMPARATIV PRIVIND

SITUAŢIILE FINANCIARE DIN

CONTABILITATEA ANGLO-SAXONĂ ŞISITUAŢIILE FINANCIARE DIN

CONTABILITATEA ROMÂNEASCĂ

Conf. univ. dr. Nicolae ECOBICIUniversitatea “Constantin Brâncuşi” din

Târgu-Jiu

Rezumat:

The two accounting systems, the French and Anglo-Saxon, tend to harmonize. We will present the financial statements of Romania, subject to OMFP

3055/2009, in parallel with the Anglo-Saxon accounting system. The issues considered are related to the reference period and the shape, structure and content of financial statements.

Cuvinte cheie: contabilitate, situa ţ ii financiare, IASB

I. Introducere

În prezent, pe plan mondial, seutilizează două sisteme de contabilitate, celfrancez şi cel anglo-saxon, respectiv două referenţiale internaţionale, cel emis de IASBşi cel emis de FASB, înregistrându-se oevidentă tendinţă de armonizare a acestora.Prin urmare, se utilizează tot mai des altereferenţiale decât cele naţionale în elaborarea

situaţiilor financiare. De exemplu, multe dinîntreprinderile mari franceze aplică normeleamericane US GAAP pentru elaborareasituaţiilor financiare, iar altele (nu numai dinFranţa) prezintă atât situaţii financiareconforme cu reglementările naţionale cât şisituaţii financiare conforme cu principiilegeneral acceptate de către Statele Unite aleAmericii (denumite US GAAP).

În ţările în care contabilitatea este slabreglementată întreprinderile adoptă normele

COMPARATIVE STUDY OF FINANCIAL

STATEMENTS IN ANGLO-SAXON AND

ROMANIAN ACCOUNTING

Assoc. Prof. PhD Nicolae ECOBICI„Constantin Brâncuşi” University of Târgu Jiu

Abstract:

The two accounting systems, the French and Anglo-Saxon, tend to harmonize. We will present the financial statements of Romania, subject to OMFP

3055/2009, in parallel with the Anglo-Saxon accounting system. The issues considered are related to the reference

period and the shape, structure and content of financial statements.

.Key words: accounting, financial statements,

International Accounting Standards Board

I. Introduction

Two accounting systems are currentlyused throughout the world, the French and theAnglo-Saxon, namely two internationalreference frames, one issued by the IASB andone issued by FASB, with an obvioustendency to harmonize them. Therefore,reference frames other than the national onesare increasingly used in preparing financialstatements. For example, many large Frenchfirms apply the American standards USGAAP for preparing financial statements, andothers (not only in France) submit bothfinancial statements in accordance withnational regulations and financial statementsin accordance with principles generallyaccepted by the United States of America(known as US GAAP).

In countries where accounting is

poorly regulated, firms adopt international or

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 2/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

134

internaţionale sau americane, în schimb înţări precum Marea Britanie, puţine sunt celecare fac referire la alte principii decât celenaţionale.

Normele contabile internaţionaleemise de IASB (International AccountingStandards Board) întâlnite sub acronimulIFRS (International Financial ReportingStandards) se aplică în prezent în multe stateale lumii inclusiv în statele membre aleUniunii Europene (UE), Hong Kong,Australia, Rusia, Africa de Sud, Singapore şiPakistan. Aproximativ 100 de state impun sau

permit utilizarea IFRS sau au o politică deconvergenţă spre acestea.

Toate societăţile comerciale cotate dinUE sunt obligate în prezent să întocmească situaţii financiare consolidate în conformitatecu IFRS. Pentru a fi aprobate pentru utilizareaîn UE, standardele trebuie să fie avizate decătre Comitetul de Reglementare Contabilă (ARC), care este format din reprezentanţi aiguvernelor statelor membre şi este consiliatde un grup de exper ţi denumit GrupulConsultativ European pentru RaportareaFinanciar ă (EFRAG). Două secţiuni din

standardul IAS 39 ”Instrumente financiare:recunoaştere şi evaluare” nu au fost aprobatede ARC şi, în această privinţă, standardeleIFRS aplicate în UE sunt diferite de celeemise de IASB. În prezent, IASB colaborează cu UE pentru a găsi o cale acceptabilă pentrueliminarea acestei anomalii.

În ceea ce priveşte convergenţa cu USGAAP, în cadrul unei reuniuni desf ăşurate în2002 la Norwalk, Connecticut, IASB şiFinancial Accounting Standards Board dinStatele Unite ale Americii (FASB) auconvenit să îşi armonizeze agendele şi să coopereze în vederea reducerii diferenţelor dintre IFRS şi Principiile Contabile GeneralAcceptate din SUA (US GAAP). În februarie2006, FASB şi IASB au semnat unMemorandum de Înţelegere care conţine un

program al aspectelor asupra cărora celor două organisme intenţionează să obţină convergenţa până în 2008. Comisia Valorilor

Mobiliare şi Burselor din Statele Unite (SEC)

American standards; however in countriessuch as Britain, few are those which refer to

principles other than the national ones.The international accounting

standards issued by IASB (InternationalAccounting Standards Board) found under the acronym IFRS (International FinancialReporting Standards) are currentlyimplemented in many countries of the worldincluding in the Member States of theEuropean Union (EU), Hong Kong, Australia,Russia, South Africa, Singapore and Pakistan.Approximately 100 countries require or allowthe use of IFRS or have a convergence policytowards them.

All EU listed companies are currentlyrequired to prepare consolidated financialstatements in accordance with IFRS. To beapproved for use in the EU, standards must

be approved by the Accounting RegulatoryCommittee (ARC), which is composed of representatives of member statesgovernments and is advised by an expertgroup called the European FinancialReporting Advisory Group (EFRAG). Twosections of IAS 39 “Financial instruments:

recognition and measurement” were notapproved by ARC and in this respect, theIFRS standards implemented in the EU aredifferent from those issued by the IASB.Currently, the IASB cooperates with the EUto find an acceptable way to address thisanomaly.

With regard to the convergence withUS GAAP, in a meeting held in 2002 in

Norwalk, Connecticut, IASB and FinancialAccounting Standards Board of the UnitedStates of America (FASB) agreed toharmonize their agendas and work together toreduce differences between IFRS and theGenerally Accepted Accounting Principles of USA (US GAAP). In February 2006, FASBand IASB signed a Memorandum of Understanding which contains a schedule of the matters over which the two organizationsintend to achieve convergence by 2008. TheSecurities and Exchange Commission in the

United States (SEC) now requires all foreign

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 3/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

135

impune în prezent tuturor companiilor str ăinecotate la burse din SUA să pregătească situaţii financiare fie în conformitate cu USGAAP, fie în conformitate cu standardele lor

contabile locale, însoţite de o notă care să reconcilieze standardele locale cu US GAAP.Această obligaţie generează costurisemnificative pentru companiile cotate înacelaşi timp în SUA şi în alte ţări. SEC a

propus modificarea acestei reguli în sensuleliminării obligaţiei de a efectua oreconciliere cu US GAAP pentru companiilestr ăine care îşi pregătesc situaţiile financiareîn conformitate cu IFRS, în principiuîncepând din 2009. Companiile bazate în

SUA sunt în continuare obligate să raportezeîn conformitate cu US GAAP.

Vom prezenta în continuare situaţiilefinanciare din România, reglementate prinOMF 3055 din 29.10.2009, în paralel cu celedin contabilitatea în sistem anglo-saxon.Aspectele avute în vedere sunt referitoare la

perioada de referinţă, pe de o parte, şi laforma, structura şi conţinutul situaţiilor financiare, pe de altă parte.

II. Perioada de referinţă utilizată la întocmirea situaţiilor financiare

Companiile, întreprinderile,instituţiile, societăţile de orice fel şi mărime,

persoanele juridice din întreaga lumeîntocmesc „conturi” şi situaţii financiare

pentru a fi prezentate utilizatorilor deinformaţii, proprietarilor, controlorilor,administratorilor, organelor fiscale, după ometodologie unică - iar aceasta estecontabilitatea. Deciziile economice care suntluate de utilizatorii situaţiilor financiarenecesită evaluarea capacităţii unei instituţii dea genera numerar sau echivalente alenumerarului şi a perioadei şi siguranţeigener ării lor. În ultimă instanţă de aceastadepinde, de exemplu, capacitatea ei de a-şi

plăti angajaţii şi furnizorii, de a plăti dobânzi,de a rambursa credite şi de a realiza

programele administrative. Utilizatorii sunt

mai în măsur ă să evalueze această capacitate

companies listed on U.S. exchanges to prepare financial statements either incompliance with US GAAP or in compliancewith their local accounting standards,

accompanied by a note reconciling localstandards with US GAAP. This requirementcreates significant costs for the companieslisted in the same time in the U.S. and inother countries. SEC has proposed to amendthis rule in order to remove the obligation tocarry out reconciliation with US GAAP for foreign companies preparing their financialstatements in accordance with IFRS, in

principle since 2009. Companies based in theU.S. are still obliged to report in compliance

with the US GAAP. Next we will present the financial

statements of Romania, regulated by theOMF 3055 of 29/10/2009, alongside theAnglo-Saxon accounting system. The issuesconsidered are related to the reference period,on the one hand, and to the shape, structureand content of financial statements, on theother hand.

II. The reference period used inpreparing financial statements

Companies, enterprises, institutions,companies of every kind and size, legal

persons around the world prepare “accounts”and financial statements to be submitted tousers of information, owners, controllers,administrators, fiscal authorities, based on aunique methodology - namely, theaccounting. The economic decisions taken byusers of financial statements require theevaluation of an institution’s ability togenerate cash or cash equivalents, andevaluation of their generation period andsafety. Ultimately, for example, its ability to

pay employees and suppliers, to pay interest,to repay loans and to carry out administrative

programs depends on it. Users are more likelyto assess this ability to generate cash or cashequivalent if they are offered informationfocused on the financial position,

performance and changes in the financial

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 4/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

136

de a genera numerar sau echivalente alenumerarului dacă le sunt oferite informaţiiconcentrate asupra poziţiei financiare,

performanţei şi modificărilor poziţiei

financiare a instituţiei.Pentru a satisface nevoile de informare privind poziţia, performanţa şi gestionareaeconomică a oricărei entităţi, se impune canecesitate, sintetizarea periodică a activităţiientităţii şi supunerea acesteia unei analize defond prin intermediul situaţiilor financiare. Prinurmare, situaţiile financiare se întocmesc lasfâr şitul unei anumite perioade de referinţă.

Conform legislaţiei naţionale (Legeacontabilităţii nr. 82/1991, republicată şi

modificată), această perioadă de referinţă poartă denumirea de exerciţiu financiar (pentruentităţi economice) şi respectiv de exerciţiu

bugetar (pentru instituţii publice). În SUA,termenul cel mai utilizat pentru perioada dereferinţă a situaţiilor financiare îl reprezintă anul fiscal.

În România, exerciţiul financiar/bugetar coincide cu anul calendaristic, respectiv începela 1 ianuarie sau la data înfiinţării entităţii şi seîncheie la 31 decembrie, sau la data desfiinţării

(dizolvării) acesteia. Prin urmare, nicio entitatedin România nu are dreptul de a alege o altă

perioadă de referinţă, aceasta fiind strictreglementată prin Legea contabilităţii.

În schimb, în SUA – ca exponent allibertăţii absolute, contabilitatea anglo-saxonă

permite tuturor entităţilor să-şi aleagă momentul de închidere a anului fiscal atâtatimp cât perioada raportată în situaţiilefinanciare reprezintă aproximativ un ancalendaristic şi este constantă de la un an laaltul. Având posibilitatea alegerii perioadei dereferinţă, tot mai multe companii americaneoptează pentru închiderea anului contabil(fiscal) în acele momente care corespund unui

punct din ciclul lor anual de activitate, respectivatunci când stocurile şi activitatea lor înregistrează nivelul cel mai scăzut. Avantajele

principale al acestei alegeri constau înreducerea timpului şi efortului necesareelabor ării situaţiilor financiare. Spre exemplu,

alegând ca perioadă de referinţă sfâr şitul lunii

position of the institution.To meet the information needs regarding

the position, performance and economicmanagement of any entity, it is required as a

necessity to periodically synthesize the businessof the entity and its submission to aninvestigation on the ground through financialstatements. Accordingly, the financialstatements are prepared after a certain period of reference.

In compliance with national laws(Accounting Law no. 82/1991, republishedand amended), this reference period is calledfinancial year (for economic entities) and

budgetary year (for public institutions). In the

U.S.A, the term most frequently used for thereference period of financial statements is thefiscal year.

In Romania, the financial / budgetary year coincides with the calendar year that begins onJanuary 1 or after the incorporation date of theentity and ends on December 31, or on itsdissolution date. Therefore, no entity inRomania is entitled to choose a differentreference period, which is strictly regulated bythe Accounting Law.

Instead, in the U.S.A - as an exponent of absolute freedom, the Anglo-Saxon accountingallows all entities to choose when to close thefiscal year as long as the period reported infinancial statements is approximately onecalendar year and is constant from one year toanother. Given the possibility to choose thereference period, more and more Americancompanies choose to close the accounting(fiscal) year at the time corresponding to a pointin their annual activity cycle, that is when their inventories and activity are at the lowest levels.The main advantages of this choice lie inreducing the time and effort required to preparethe financial statements. For example, choosingthe end of January as the reference period,which coincides with liquidation of inventoriesat reduced prices, the American companies caninventorize their stocks much cheaper andfaster and their managers can give more time tothe operations processing the accounting

information as they are no longer needed too

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 5/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

137

ianuarie, perioadă ce coincide cu lichidareastocurilor la preţ redus, companiile americane

pot inventaria mult mai ieftin şi rapid stocurile,iar managerii acestora pot acorda mai mult timp

operaţiunilor privind prelucrarea informaţiilor contabile întrucât nu mai sunt atât de solicitaţide conducerea activităţii de bază a entităţii.Există şi companii americane care nu încheieanul fiscal în aceeaşi dată în fiecare an întrucâtacesta (anul fiscal) cuprinde un anumit număr de zile sau de să ptămâni, iar altele aleg ca dată de închidere a anului fiscal o anumită zi dinsă ptămâna cea mai apropiată de o anumită dată (spre exemplu, ultima duminică din lunaseptembrie a fiecărui an, etc.).

III. Forma, structura şi conţinutulsituaţiilor financiare

Forma, structura şi conţinutul situaţiilor financiare întocmite de entităţile din Româniasunt legiferate de Ordinul ministrului finanţelor

publice nr. 3055 din 29.10.2009 pentruaprobarea Reglementărilor contabileconforme cu directivele europene. Formasituaţiilor financiare întocmite conform

acestei reglementări este cea verticală, formă ce este de altfel preferată nu numai în UE câtşi în SUA. Există însă şi state europene careadoptă formatul orizontal al bilanţului ca şicomponentă a situaţiilor financiare, precumGermania şi Italia, însă utilizează doar formatul vertical pentru contul de profit şi

pierdere (altă componentă importantă asituaţiilor financiare). În consecinţă, formasituaţiilor financiare întocmite conformlegislaţiei naţionale nu difer ă de formasituaţiilor financiare întocmite conformnormelor US GAAP.

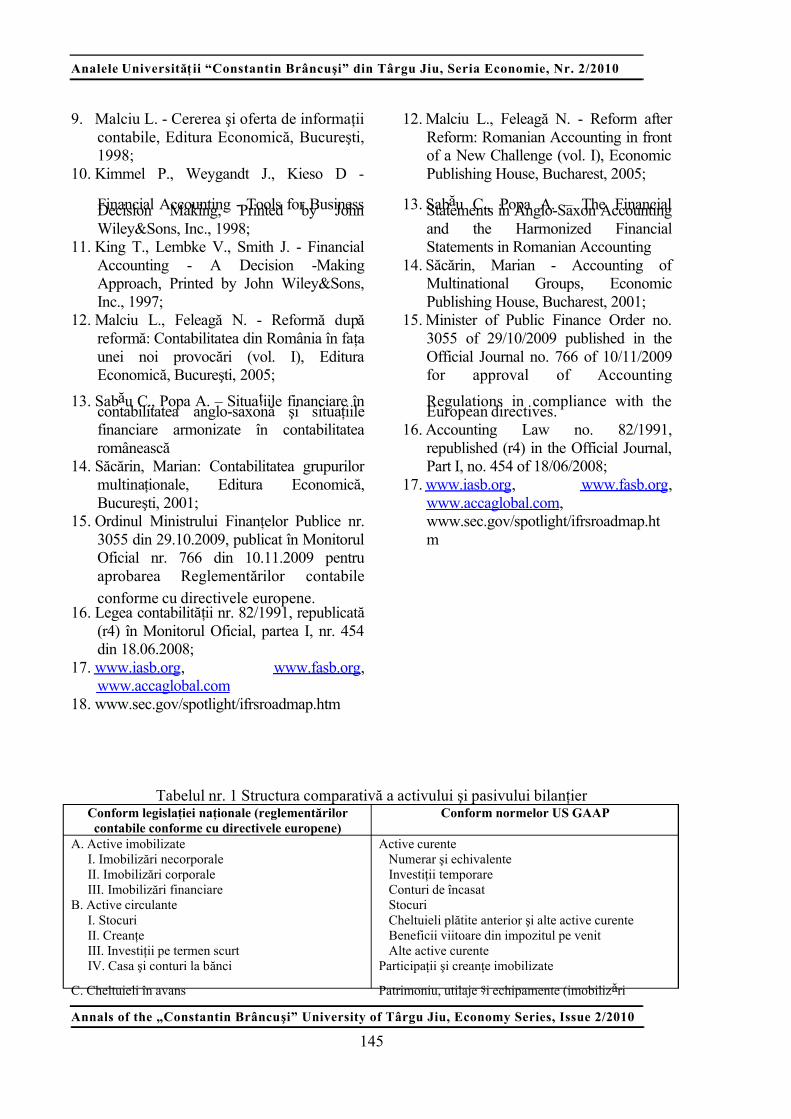

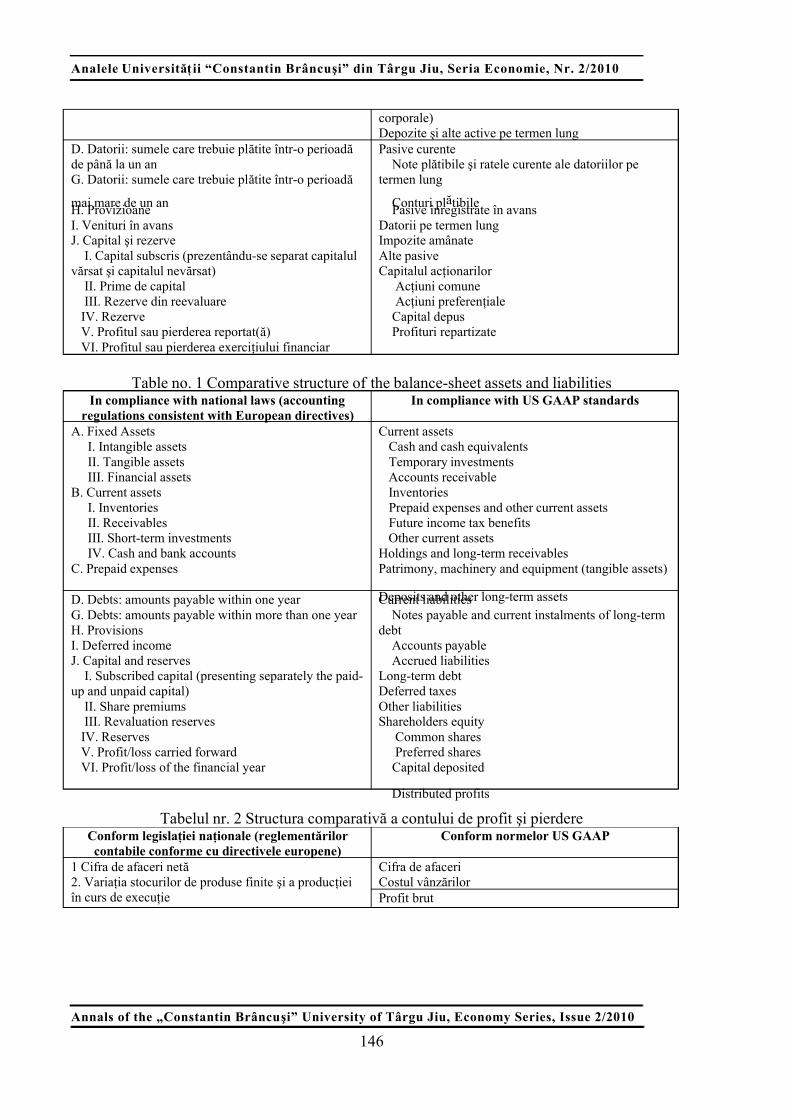

În ceea ce priveşte structura situaţiilor financiare vom ar ăta în continuare că aceastadifer ă. Astfel, conform legislaţiei naţionale(OMFP 3055/2009), situaţiile financiare

prevăd o structur ă a bilanţului care ordonează activele în ordinea crescătoare a lichidităţii,iar pasivele în ordinea crescătoareexigibilităţii. Conform normelor US GAAP,

activele sunt ordonate în bilanţ în ordine

much by the main activity management of theentity. There are also American companies thatdo not end the fiscal year in the same timeevery year, as it (the fiscal year) is made up of a

certain number of days or weeks, while otherschoose as the fiscal year closing date a certainday of the week closest to a certain date (for example, last Sunday in September each year,etc.).

III. Form, structure and content of financial statements

The form, structure and content of financial statements prepared by Romanian

entities are regulated by the Minister of PublicFinance Order no. 3055 of 29/10/2009 for approval of Accounting Regulations incompliance with the European directives. Theform of financial statements prepared under this regulation is vertical; in fact this shape is

preferred not only in the EU but also in theUSA. However, there are European countriesthat adopt the horizontal format of the

balance sheet as part of the financialstatements, such as Germany and Italy, but

they use only the vertical format for the profitor loss account (another important componentof the financial statements). Consequently,the form of financial statements prepared inaccordance with national laws is no differentfrom the financial statements preparedaccording to US GAAP standards.

As for the structure of financialstatements, it differs, as we will show next.Thus, in compliance with national laws(OMFP 3055/2009), financial statements

provide a balance sheet structure that ranksassets in the increasing order of cash andliabilities in the increasing order of exigibility. According to the US GAAPstandards, assets are ranked in the balance sheetin descending order and liabilities in ascendingorder. Synthetically, these differences can beseen in table no. 1.

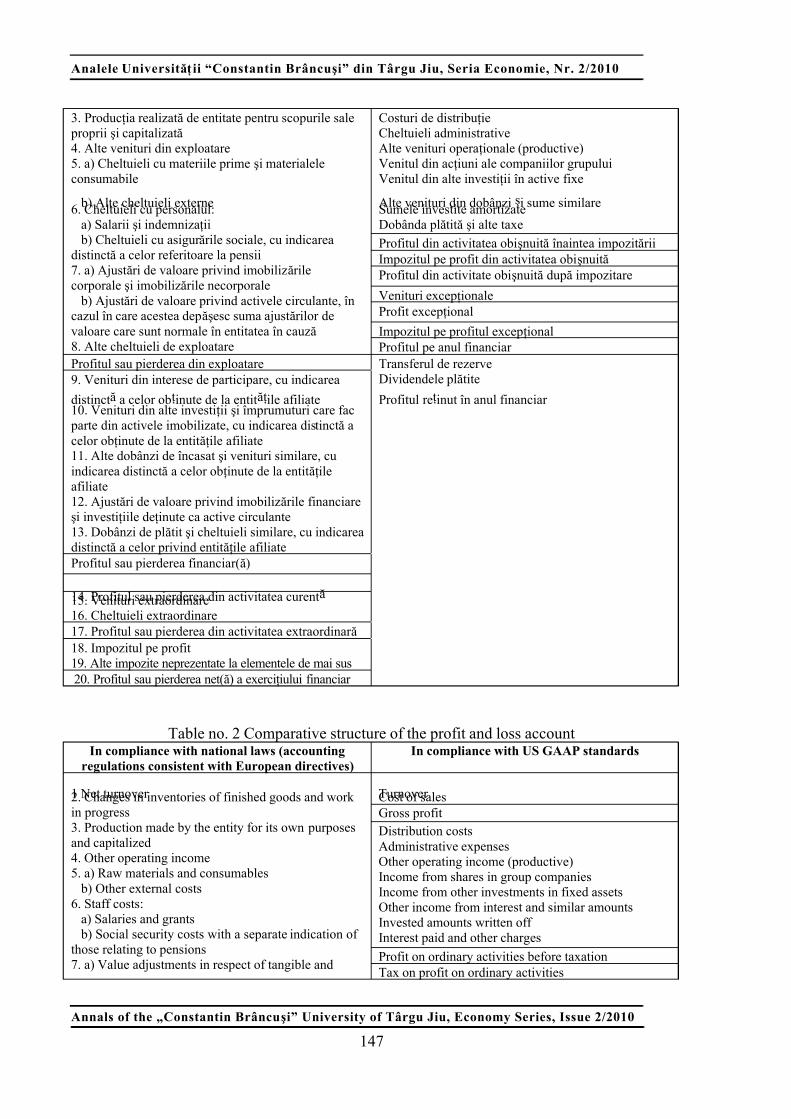

In compliance with the national laws,the profit and loss account includes all

revenues and expenses of the year, grouped

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 6/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

138

descrescătoare, iar pasive în ordine crescătoare.Sintetic, aceste diferenţe se observă în tabelulnr. 1.

Conform legislaţiei naţionale, contul

de profit şi pierdere cuprinde toate veniturileşi cheltuielile exerciţiului financiar, grupatedupă natura lor, dispuse alternativ (venituri şiapoi cheltuieli în cadrul fiecărei activităţi, custabilirea rezultatului pe fiecare activitate),

precum şi rezultatul exerciţiului. Conformnormelor US GAAP, activitatea de exploataredin contul de profit şi pierdere este structurată diferit, cheltuielile de exploatare fiindordonate atât în funcţie de natur ă cât şi înfuncţie de destinaţia lor economică, iar

anumite venituri şi cheltuieli pot fi prezentatecumulat. Sintetic, aceste diferenţe se observă întabelul nr. 2.

În privinţa „Situaţiei fluxurilor denumerar (sau de trezorerie)” am constatat că atât varianta românească (conformă cudirectivele europene) cât şi cea americană

prezintă aceeaşi structur ă, folosindu-se unuldin modelele prezentate de IAS 7 (variantadirectă sau cea indirectă).

Cât priveşte „Situaţia modificărilor

capitalului propriu”, varianta românească relevă în patru momente (sold la începutulexerciţiului, creşteri, reduceri şi sold lasfâr şitul exerciţiului) toate elementele decapitaluri proprii:¾ Ccapitalul subscris/patrimoniul regiei;¾ Pprime de capital;¾ Rrezerve (Rezerve din reevaluare,

Rezerve legale, Rezerve statutare saucontractuale, Rezerve reprezentândsurplusul realizat din rezerve dinreevaluare, Alte rezerve);

¾ Acţiuni proprii;¾ Câştiguri legate de instrumentele de

capitaluri proprii;¾ Pierderi legate de instrumentele de

capitaluri proprii;¾ Rezultat reportat (Rezultatul reportat

reprezentând profitul nerepartizat sau pierderea neacoperită, Rezultatul reportat provenit din adoptarea pentru prima dată

a IAS, mai puţin IAS 29, Rezultatul

by their nature, arranged alternately (revenue,then expenses within each activity,establishing the earnings per each activity),and the profit or loss for the period.

According to US GAAP, the operatingactivity in the profit and loss account isstructured differently, the operating costs areordered both by nature and according to their economic destination and certain revenue andexpenses can be presented cumulatively.Synthetically, these differences can be seen intable no. 2.

In the “Cash flow statement (or treasury)” I found that the Romanian version(in line with European directives) and the

American one have the same structure, usingone of the models presented in IAS 7 (director indirect version).

As for the “Statement of changes inequity”, the Romanian version shows in four moments (balance at beginning of the year,increases, reductions and balance at the year end) all the equity items:¾ Subscribed capital / patrimony

(autonomous companies);¾ Share premiums;¾ Reserves (Revaluation reserves, Legal

reserves, Statutory or contractual capitalreserves, Reserve representing therevaluation reserve surplus, Other reserves);

¾ Own shares;¾ Earnings associated to equity

instruments;¾ Losses associated to equity instruments;¾ Retained Earnings (Profit/loss carried

forward, Retained earnings due to thefirst time adoption of IAS, except IAS29, Retained earnings due to thecorrection of accounting errors, Retainedearnings due to the enforcement of theAccounting Regulations consistent withthe 4th Directive of the EuropeanEconomic Communities);

¾ Profit/loss of the financial year;¾ Profit distribution¾ Total equity.

In the American version, “Equity

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 7/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

139

reportat provenit din corectarea erorilor contabile, Rezultatul reportat provenit dintrecerea la aplicarea Reglementărilor contabile conforme cu Directiva a IV-a a

Comunităţilor Economice Europene);¾ Profitul/pierderea exerciţiului financiar;¾ Repartizarea profitului¾ Total capitaluri proprii.

În varianta americană, „Situaţiamodificării capitalului” cuprinde două păr ţi:situaţia repartizării profitului şi situaţiaacţiunilor. Există şi o alternativă la această situaţie, denumită „Situaţia repartizării

profitului”, însă prima situaţie este preferată de companiile americare întrucât conţine atât

factorii care au determinat modificareasituaţiei capitalurilor în timpul perioadei, câtşi a acelora care au determinat modificări înrepartizarea profitului.

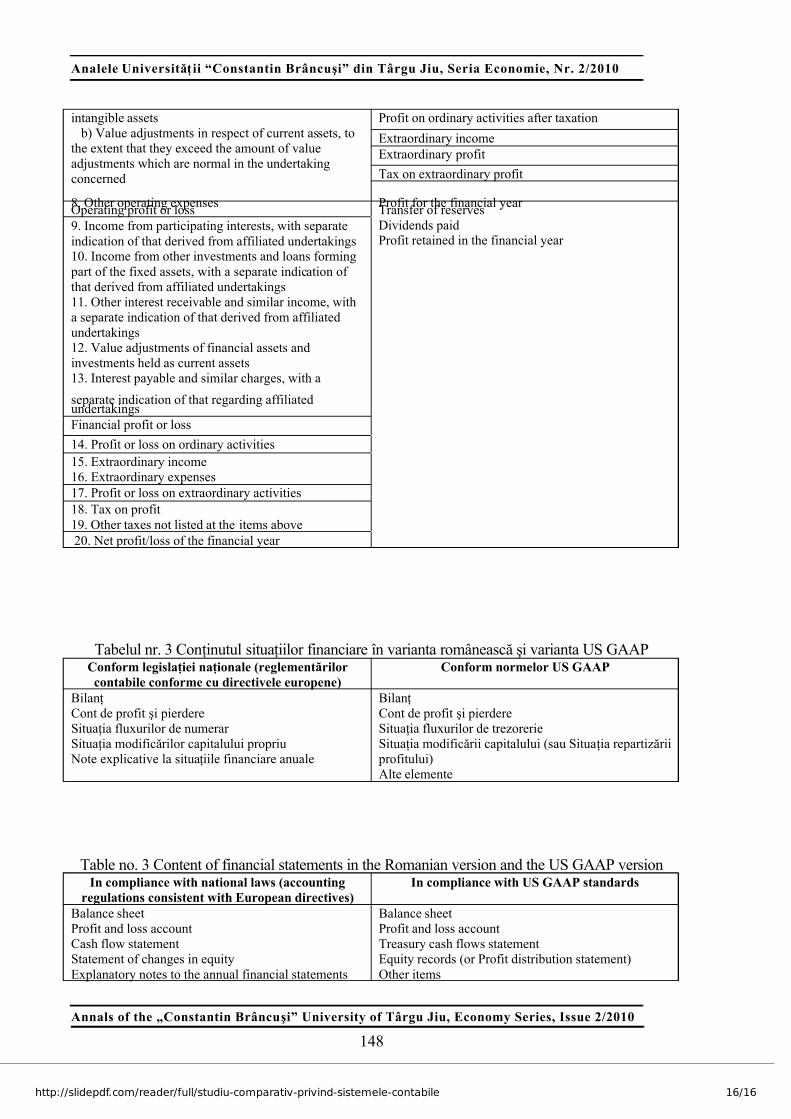

Dacă până în acest punct, conţinutulsituaţiilor financiare, în ambele variante, esteaproximativ acelaşi, diferind câteodată structura acestora (forma, ordonareaelementelor etc.), ultima componentă difer ă şica denumire cât şi ca formă. Este vorba decea de-a cincea (ultima) componentă a

situaţiilor financiare, denumită „Noteexplicative la situaţiile financiare anuale” învarianta românească conformă cu directiveleeuropene, respectiv „Alte elemente” învarianta US GAAP. În ambele variante,această ultimă componentă este destinată utilizatorilor în vederea relevării informaţiilor suplimentare necesare unei informări cât maicomplete privind poziţia financiar ă şirezultatele obţinute ale entităţii.

În varianta românească, „Noteleexplicative la situaţiile financiare anuale”exemplifică modul de prezentare ainformaţiilor prin celelalte componente alesituaţiilor financiare. Ca urmare, entităţilestabilesc formatul notelor explicative, cucondiţia prezentării cel puţin a informaţiilor solicitate, referitoare la elementele cuprinseîn situaţiile financiare anuale. Prin urmare,entităţile sunt obligate să întocmească noteexplicative (cel puţin 10 la număr) care să

acopere toate informaţiile necesar a fi

records” is made of two parts: profitdistribution statement and statement of shares. There is an alternative to thisstatement, the “Profit distribution statement”,

but the first one is preferred by the Americancompanies as it contains both the factors behind the changes in the equity recordsduring the period and those that causedchanges in profit distribution.

If by this point, the content of financial statements in both versions is aboutthe same, sometimes their structure (form,items ordering, etc.) differs; the lastcomponent is different both in name andform. This is the fifth (last) part of the

financial statements, called “Explanatorynotes to the annual financial statements” inthe Romanian version consistent withEuropean directives, namely “Other elements” in the US GAAP version. In bothvariants, this last component is intended tousers for disclosure of additional informationnecessary for comprehensive information onthe financial position and earnings of theentity.

In the Romanian version, the

“Explanatory notes to the annual financialstatements” illustrate how disclosure aremade through the other components of financial statements. As a result, the entitiesestablish the format of explanatory notes,

provided that at least the informationrequested, regarding the items contained inthe annual financial statements, is submitted.Therefore, entities are required to prepareexplanatory notes (at least 10 in number)covering all the information to be submittedon:¾ Fixed assets;¾ Provisions;¾ Profit distribution;¾ Analysis of the operating profit/loss;¾ Statement of receivables and debts;¾ Principles, policies and accounting

methods;¾ Holdings and financing sources;¾ Information on employees and

members of the administration,

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 8/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

140

prezentate, privind:¾ Active imobilizate;¾ Provizioane;¾ Repartizarea profitului;

¾ Analiza rezultatului din exploatare;¾ Situaţia creanţelor şi datoriilor;¾ Principii, politici şi metode contabile;¾ Participaţii şi surse de finanţare;¾ Informaţii privind salariaţii şi membrii

organelor de administraţie, conducere şide supraveghere;

¾ Exemple de calcul şi analiză a principalilor indicatori economico-financiari;

¾ Alte informaţii.

În varianta americană, această ultimă componentă a situaţiilor financiare („Alteelemente”), f ăr ă de care nicio analiză aacestora n-ar fi completă, cuprinde:¾ discuţia şi analiza managerilor. Această

situaţie cuprinde la rândul ei trei aspectefinanciare ale companiei, şi anume:capacitatea de a rambursa obligaţiile petermen scurt, capacitatea de a asigurafondurile necesare pentru activitateacurentă şi pentru extindere, respectiv

rezultatele obţinute;¾ note la situaţiile financiare. Acestea

furnizează detalii suplimentare despreinformaţiile prezentate în situaţiilefinanciare de bază;

¾ raportul de audit. Dacă auditorul îşiexprimă o părere calificată privind

poziţia financiar ă, rezultatele activităţiişi fluxurile de trezorerie prezentate însituaţiile financiare, în sensul că emulţumit de felul în care acestea sunt înconcordanţă cu normele US GAAP,atunci aceste situaţii financiare pot fiutilizate f ăr ă restricţii de cătreutilizatorii informaţiilor cuprinse înacestea. În cazul în care auditorul îşiexprimă rezerve, atunci informaţiicuprinde în situaţiile financiare auditate

pot fi utilizate numai cu anumiterestricţii.

management and supervisionauthorities;

¾ Examples of calculation and analysis of the main economic and financial

indicators;¾ Other information.

In the American version, this lastcomponent of the financial statements(“Other items”), without which no suchanalysis would be complete, includes:¾ managers’ discussion and analysis. In

its turn, this statements contains threefinancial aspects of the company,namely: ability to repay short-termobligations, the ability to provide the

necessary funds for current activitiesand expansion, i.e. the earningsobtained;

¾ notes to the financial statements. They provide further details about theinformation presented in the basicfinancial statements;

¾ audit report. If the auditor expresses aqualified opinion on the financial

position, earnings and cash flows presented in the financial statements,

meaning that he is satisfied with theway they are consistent with the USGAAP standards, then these financialstatements can be used withoutrestrictions by the users of theinformation contained therein. If theauditor expresses reservations, then theinformation from the financialstatements audited may be used onlywith certain restrictions.

IV. Conclusions and proposals

The position, performance andfinancial management of an entity (public,economic, commercial, administrativeinstitutions etc.) necessarily require that their work is periodically synthesized, undergoingan investigation on the ground through thefinancial statements. As stipulated in Art. 10

paragraph 1 of the Accounting Law no.

82/1991 (republished and amended) “the

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 9/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

141

IV. Concluzii şi propuneri

Poziţia, performanţa şi gestionareafinanciar ă a oricărei entităţi (instituţii publice,

economico – comerciale, administrative etc.)impun în mod necesar, ca periodic activitateaacestora să fie sintetizată şi supusă uneianalize de fond prin intermediul situaţiilor financiare. Aşa cum precizează art. 10, al. 1al Legii contabilităţii nr. 82/1991 (republicată şi modificată) „documentele oficiale de

prezentare a situaţiei economico – financiarea persoanelor juridice prevăzute la art. 1(societăţi comerciale, instituţii publice,asociaţii şi organizaţii, etc.) sunt situaţiile

financiare anuale, stabilite potrivit legii, caretrebuie să ofere o imagine fidelă a poziţieifinanciare, performanţei financiare şi acelorlalte informaţii referitoare la activitateadesf ăşurată”. Situaţiile financiare seîntocmesc pornind de la conturile curente,supuse verificării prin intermediul balanţei deverificare, întocmite cel puţin anual, sau latermenele de întocmire a situaţiilor financiare

periodice. Situaţiile financiare sunt un complex

de sinteze specific contabile, situaţii, anexe,calcule comparative, fiecare cu explicitareaconducerii, discutate şi aprobate subsemnătur ă de organele abilitate, supuseauditării şi f ăcute publice. Aceste„formalizări” au menirea de a întări valoareacognitivă a informaţiilor contabileconcomitent cu valorificarea lor în procesuldecizional şi managerial.

În contextul golbalizării şiinternaţionalizării, situaţiile financiare pot fiîntocmite având la bază norme interne(legislaţia naţională) sau norme internaţionale(IFRS şi US GAAP).

Am prezentat pe parcursul acesteilucr ări asemănările şi deosebirile privindelaborarea situaţiilor financiare anuale învarianta americană (US GAAP) şi în variantaromânească (conformă integral cu directiveleeuropene începând cu situaţiile financiareîntocmite pentru anul 2010), prin prisma a două

aspecte: perioada de referinţă, pe de o parte, şi

official documents presenting the economicand financial statement of legal personsreferred to in Art. 1 (companies, publicinstitutions, associations and organizations,

etc.) are annual financial statements,established by law, which have to provide afair view of the financial position, financial

performance and of the other informationrelated to the activity carried out”. Financialstatements are drawn from current accounts,subject to verification by the verification

balance sheet, prepared at least annually, or on the deadlines set for preparing periodicfinancial statements.

Financial statements are a complex of

accounting specific syntheses, statements,annexes, comparative calculations, each withthe management explanation, discussed andapproved under signature by the authorized

bodies, subject to auditing and made public.These “formalizations” are designed toenhance cognitive value of accountinginformation together with its application indecision making and management process.

In the context of globalization andinternationalization, financial statements can be

made based on national standards (nationallaws) or international standards (IFRS and USGAAP).

Throughout this paper we have shownthe similarities and differences on the

production of annual financial statements in theAmerican version (US GAAP) and in theRomanian version (fully consistent withEuropean directives starting with the financialstatements prepared for 2010), considering twoaspects: the reference period, on the one hand,and form, structure and content, on the other hand.

We can certainly say that theRomanian system (as the European one) doesnot allow the choice of the reference period for

preparing annual financial statements (thecalendar year coincides with the financial year).However, American companies have completefreedom on this subject, their only obligation inchoosing the reference period referring to the

reference (reported) period is to represent

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 10/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

142

forma, structura şi conţinutul, pe de altă parte.Putem spune cu siguranţă că sistemul

românesc (ca şi cel european de altfel) nu permite alegerea perioadei de referinţă pentru

elaborarea situaţiilor financiare anuale (anulcalendaristic coincide cu exerciţiul financiar).În schimb, o libertate deplină privind acestsubiect o au companiile americane, singuraobligaţie a acestora în alegerea perioadei dereferinţă referindu-se la perioada de referinţă (raportată) să reprezinte aproximativ un ancalendaristic şi să fie constantă de la un an laaltul.

Din punct de vedere al conţinutuluisituaţiilor financiare, ambele variante cuprind

cinci componente, aşa cum se poate observa întabelul nr. 3.Cât priveşte forma, aşa cum am prezentat lacapitolul III, ambele variante folosesc formaverticală.

În ceea ce priveşte structura situaţiilor financiare am ar ătat că între cele două variante există şi diferenţe (ordinea

prezentării elementelor bilanţiere etc.), dar şiasemănări.

Având în vedere faptul că legislaţia

românească prevede ca situaţiile financiareanuale fie auditate şi să fie însoţite de odeclaraţie scrisă de asumare a r ăspunderiiconducerii persoanei juridice pentru întocmireaacestora în conformitate cu Reglementărilecontabile conform cu Directiva a IV-a aComunităţilor Economice Europene,concluzionăm că informaţiile cerute de ambelevariante a fi cuprinse în cadrul situaţiilor financiare anuale sunt relevante, complete subtoate aspectele semnificative şi credibile,

prezentând fidel rezultatele şi poziţia financiar ă aentităţii.

Altfel spus, cu toate deosebirile existenteîntre cele două variante, putem spune că procesulde armonizare se găseşte în prezent într-o fază accentuată, fapt demonstrat şi prin faptul că legislaţia naţională a implementat referenţialulIASB, referenţial aflat la rândul său în stadiuaccentuat de armonizare cu referenţialul FASB

approximately one calendar year and beconsistent from one year to another.

As to the content of financialstatements, both versions include five

components, as can be seen in table no. 3.

As to form, as shown in Chapter III, bothversions use the vertical form.

Regarding the structure of financialstatements, we showed that between the twoversions there are differences (order of

presentation of balance sheet items, etc.), butalso similarities.

Given that the Romanian law requiresthe annual financial statements to be audited1

and accompanied by a written declaration toassume responsibility of the legal person'smanagement for preparing them in accordancewith the Accounting Regulations consistent withthe 4th Directive of the European EconomicCommunities, we can draw the conclusion thatthe information required by both versions to beincluded in the annual financial statements arerelevant, complete in all the significant respectsand reliable, accurately presenting the resultsand financial position of the entity.

In other words, despite the differences between the two versions, we can say that the process of harmonization is now in a strong phase, as demonstrated by the fact that thenational laws have implemented the IASBreference frame, which is also in advancedstage of harmonization with the reference frameFASB (US GAAP). In a mathematicalexpression, if speaking in principle, nationallaws are in line with IASB reference frame,which is consistent with the reference frameFASB, then the national laws are consistentwith the reference frame FASB (q.e.d.)

However, even if the content of financial statements in Romania hasimproved, meaning that they also include a

picture of cash flows and a statement of changes in equity, however, we can not saythat the harmonization process wasconcluded, because the usefulness of the

1 Excepted from the audit are the simplified annual financial statements, as defined in OMFP no. 3055/2009.

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 11/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

143

(US GAAP). Într-o exprimare matematică, dacă, principial vorbind, legislaţia naţională esteconformă cu referenţialul IASB, iar referenţialulIASB este conform cu referenţialul FASB, atunci

legislaţia naţională este conformă cu referenţialulFASB (q.e.d.)Cu toate acestea, chiar dacă în România

conţinutul situaţiilor financiare s-aîmbunătăţit, în sensul că acestea cuprind şi untablou al fluxurilor de numerar şi o situaţie amodificărilor capitalurilor proprii, totuşi nu

putem afirma că procesul de armonizare s-aîncheiat, deoarece utilitatea informaţiilor cuprinse în situaţiile financiare depinde, maiales, de calitatea acestora, şi nu doar la

cantitatea lor.Prin urmare, calitatea informaţiilor

cuprinse în situaţiile financiare elaborateconform legislaţiei naţionale mai pot fiîmbunătăţite sau ameliorate în vedereacreşterii credibilităţii lor. Prezentăm încontinuare câteva modalităţi de perfecţionarea conţinutului şi calităţii informaţiilor cuprinse în situaţiile financiare.

În primul rând, este absolut necesar cautilizatorii informaţiilor contabile să

beneficieze şi de informaţii previzionale subforma bugetelor sau previziunilor, având învedere că informaţiile conţinute în situaţiilefinanciare se refer ă la trecut, iar deciziileutilizatorilor au în vedere viitorul. Referenţialulamerican rezolvă această problemă prin ultimacomponentă („Alte elemente”, în principal însecţiunea „Discuţii şi analize manageriale”).

În acelaşi spirit al perfecţionării,subliniem necesitatea prezentării în situaţiilefinanciare (varianta românească) a unor informaţii speciale pentru salariaţi, care să fieconţinute într-un aşa numit bilanţ social,document care se întocmeşte în prezent înFranţa spre exemplu.

Nu în ultimul rând, reiter ămnecesitatea prezentării situaţiei generale aentităţii, respectiv furnizarea de informaţiidespre profilul activităţii, locul deţinut însectorul de activitate respectiv, poziţia pe

piaţă, responsabilităţile privind mediul

înconjur ător etc, toate aceste informaţii fiind

information contained in financial statementsdepends, above all, on their quality, and not

just their quantity.Therefore, the quality of the

information contained in the financialstatements prepared in accordance with thenational laws can be improved in order toincrease their credibility. You can find belowsome ways to improve the content and qualityof the information contained in the financialstatements.

First, it is imperative that users of accounting information also benefit from

provisioning information as budgets or forecasts, given that the information

contained in the financial statements relate to past, and users decisions have the future inview. The American reference frame solvesthis problem by the last component (“Other elements”, mainly in “Managerial discussionsand analysis”).In the same spirit of improvement, we are

pointing out the need to include in thefinancial statements (Romanian version)some special information for employees,which is contained in a so-called social

balance sheet, a document that is currentlymade in France for example.

Finally, we are reiterating the need tosubmit the general statement of the entity and

provide information about the profile of activity, the place held in that activity sector,the market position, environmentalresponsibilities etc.; all this information isindispensable to users of accountinginformation.

The Romanian Normalizer does notlimit the information that may be contained inthe Explanatory notes to financial statements,and even has some examples. Therefore, weconsider it the duty of the accounting

profession in Romania (CECCAR) to makeefforts to form a custom of providing all theadditional information necessary for the bestsubstantiation of decisions on behalf of thoseindicated in the financial statements (for example: social balance sheet, budgets and

forecasts, information on the general situation

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 12/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

144

absolut necesare utilizatorilor de informaţiicontabile.

Normalizatorul român nu limitează informaţiile ce pot fi cuprinse în Notele

explicative la situaţiile financiare, ba chiar prezintă şi unele exemple. Prin urmare,consider ăm că este de datoria profesieicontabile din România (CECCAR) să facă eforturi în vederea formării unei cutume

privind prezentarea tuturor informaţiisuplimentare necesare unor cât mai bunefundamentări a deciziilor pe seama celor

prezentate în situaţiile financiare (spreexemplui: bilanţul social, bugete şi

previziuni, informaţii privind situaţia

generală etc.).

Bibliografie:

1. Colasse B. - Comptabilité générale (PCG1999 et IAS), 7e édition, Ed. Economica,Paris, 2001;

2. Dr ăgan C.M. - Noile orizonturi alecontabilitatii institutiilor publice, EdituraUniversitar ă, 2009;

3. Epstein Barry J., Mirza Abbas Ali - IFRS2005 – Interpretarea şi aplicareaStandardelor Internaţionale de Contabilitateşi Raportare Financiar ă (traducere dinlimba engleză), BMT Publishing House,Bucureşti, 2005;

4. Feleagă N. (coordonator) - Contabilitateaprofundată, Editura Economică,Bucureşti, 1996;

5. Feleagă N. - Sisteme contabile comparate(ediţia a II-a), vol. I – 1999, Vol. II, III –

2000, Editura Economică, Bucureşti;6. Feleagă N., Malciu L. - Politici şi opţiuni

contabile. Fair Accounting versus BadAccounting, Editura Economică, Bucureşti,2002;

7. Feleagă N., Malciu L. - Provocărilecontabilităţii internaţionale la cumpănadintre milenii, Editura Economică,Bucureşti, 2004;

8. Feleagă, N. - Controverse contabile,Editura Economică, Bucureşti, 1996;

etc.).

Bibliography:

1. Colasse B. - Comptabilité générale(PCG 1999 et IAS), 7e édition,Economic Publishing House, Paris,2001;

2. Dr ăgan C.M. - New Horizons of Public Institutions Accounting,University Publishing House, 2009;

3. Epstein Barry J., Mirza Abbas Ali -IFRS 2005 – Interpretation andImplementation of International

Accounting Standards and FinancialReporting (Translation from English),BMT Publishing House, Bucharest,2005;

4. Feleagă N. (coordinator) - DetailedAccountancy, Economic PublishingHouse, Bucharest, 1996;

5. Feleagă N. - Compared AccountingSystems (2nd edition), vol. I – 1999,Vol. II, III – 2000, EconomicPublishing House, Bucharest;

6. Feleagă N., Malciu L. - AccountingPolicies and Options. Fair Accountingversus Bad Accounting, EconomicPublishing House, Bucharest, 2002;

7. Feleagă N., Malciu L. - InternationalAccounting Challenges at the Turn of the Millennium, Economic PublishingHouse, Bucharest, 2004;

8. Feleagă, N. - Controversies inAccounting, Economic PublishingHouse, Bucharest, 1996;

9. Malciu L. - Supply and Demand for Accounting Information, EconomicPublishing House, Bucharest, 1998;

10. Kimmel P., Weygandt J., Kieso D -Financial Accounting - Tools for Business Decision Making, Printed byJohn Wiley&Sons, Inc., 1998;

11. King T., Lembke V., Smith J. -Financial Accounting - A Decision -Making Approach, Printed by JohnWiley&Sons, Inc., 1997;

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 13/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

145

9. Malciu L. - Cererea şi oferta de informaţiicontabile, Editura Economică, Bucureşti,1998;

10. Kimmel P., Weygandt J., Kieso D -

Financial Accounting - Tools for BusinessDecision Making, Printed by JohnWiley&Sons, Inc., 1998;

11. King T., Lembke V., Smith J. - FinancialAccounting - A Decision -MakingApproach, Printed by John Wiley&Sons,Inc., 1997;

12. Malciu L., Feleagă N. - Reformă după reformă: Contabilitatea din România în faţaunei noi provocări (vol. I), EdituraEconomică, Bucureşti, 2005;

13. Sabău C., Popa A. – Situaţiile financiare încontabilitatea anglo-saxonă şi situaţiilefinanciare armonizate în contabilitatearomânească

14. Săcărin, Marian: Contabilitatea grupurilor multinaţionale, Editura Economică,Bucureşti, 2001;

15. Ordinul Ministrului Finanţelor Publice nr.3055 din 29.10.2009, publicat în MonitorulOficial nr. 766 din 10.11.2009 pentruaprobarea Reglementărilor contabile

conforme cu directivele europene.16. Legea contabilităţii nr. 82/1991, republicată

(r4) în Monitorul Oficial, partea I, nr. 454din 18.06.2008;

17. www.iasb.org, www.fasb.org,www.accaglobal.com

18. www.sec.gov/spotlight/ifrsroadmap.htm

12. Malciu L., Feleagă N. - Reform after Reform: Romanian Accounting in frontof a New Challenge (vol. I), EconomicPublishing House, Bucharest, 2005;

13. Sabău C., Popa A. – The FinancialStatements in Anglo-Saxon Accountingand the Harmonized FinancialStatements in Romanian Accounting

14. Săcărin, Marian - Accounting of Multinational Groups, EconomicPublishing House, Bucharest, 2001;

15. Minister of Public Finance Order no.3055 of 29/10/2009 published in theOfficial Journal no. 766 of 10/11/2009for approval of Accounting

Regulations in compliance with theEuropean directives.

16. Accounting Law no. 82/1991,republished (r4) in the Official Journal,Part I, no. 454 of 18/06/2008;

17. www.iasb.org, www.fasb.org,www.accaglobal.com,www.sec.gov/spotlight/ifrsroadmap.htm

Tabelul nr. 1 Structura comparativă a activului şi pasivului bilanţier Conform legislaţiei naţionale (reglementărilorcontabile conforme cu directivele europene)

Conform normelor US GAAP

A. Active imobilizateI. Imobilizări necorporaleII. Imobilizări corporaleIII. Imobilizări financiare

B. Active circulanteI. StocuriII. CreanţeIII. Investiţii pe termen scurtIV. Casa şi conturi la bănci

C. Cheltuieli în avans

Active curente Numerar şi echivalenteInvestiţii temporareConturi de încasatStocuriCheltuieli plătite anterior şi alte active curenteBeneficii viitoare din impozitul pe venitAlte active curente

Participaţii şi creanţe imobilizate

Patrimoniu, utilaje şi echipamente (imobilizări

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 14/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

146

corporale)Depozite şi alte active pe termen lung

D. Datorii: sumele care trebuie plătite într-o perioadă de până la un anG. Datorii: sumele care trebuie plătite într-o perioadă

mai mare de un anH. ProvizioaneI. Venituri în avansJ. Capital şi rezerve

I. Capital subscris (prezentându-se separat capitalulvărsat şi capitalul nevărsat)

II. Prime de capitalIII. Rezerve din reevaluare

IV. RezerveV. Profitul sau pierderea reportat(ă)VI. Profitul sau pierderea exerciţiului financiar

Pasive curente Note plătibile şi ratele curente ale datoriilor pe

termen lung

Conturi plătibilePasive înregistrate în avansDatorii pe termen lungImpozite amânateAlte pasiveCapitalul acţionarilor

Acţiuni comuneAcţiuni preferenţiale

Capital depusProfituri repartizate

Table no. 1 Comparative structure of the balance-sheet assets and liabilitiesIn compliance with national laws (accounting

regulations consistent with European directives)In compliance with US GAAP standards

A. Fixed AssetsI. Intangible assetsII. Tangible assetsIII. Financial assets

B. Current assetsI. InventoriesII. ReceivablesIII. Short-term investmentsIV. Cash and bank accounts

C. Prepaid expenses

Current assetsCash and cash equivalentsTemporary investmentsAccounts receivableInventoriesPrepaid expenses and other current assetsFuture income tax benefitsOther current assets

Holdings and long-term receivablesPatrimony, machinery and equipment (tangible assets)

Deposits and other long-term assetsD. Debts: amounts payable within one year G. Debts: amounts payable within more than one year H. ProvisionsI. Deferred incomeJ. Capital and reserves

I. Subscribed capital (presenting separately the paid-up and unpaid capital)

II. Share premiumsIII. Revaluation reserves

IV. ReservesV. Profit/loss carried forwardVI. Profit/loss of the financial year

Current liabilities Notes payable and current instalments of long-term

debtAccounts payableAccrued liabilities

Long-term debtDeferred taxesOther liabilitiesShareholders equity

Common sharesPreferred sharesCapital deposited

Distributed profits

Tabelul nr. 2 Structura comparativă a contului de profit şi pierdereConform legislaţiei naţionale (reglementărilorcontabile conforme cu directivele europene)

Conform normelor US GAAP

Cifra de afaceriCostul vânzărilor

1 Cifra de afaceri netă 2. Variaţia stocurilor de produse finite şi a producţieiîn curs de execuţie Profit brut

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 15/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

147

Costuri de distribuţieCheltuieli administrativeAlte venituri operaţionale (productive)Venitul din acţiuni ale companiilor grupuluiVenitul din alte investiţii în active fixe

Alte venituri din dobânzi şi sume similareSumele investite amortizateDobânda plătită şi alte taxe

Profitul din activitatea obişnuită înaintea impozităriiImpozitul pe profit din activitatea obişnuită Profitul din activitate obişnuită după impozitare

Venituri excepţionaleProfit excepţional

Impozitul pe profitul excepţional

3. Producţia realizată de entitate pentru scopurile sale proprii şi capitalizată 4. Alte venituri din exploatare5. a) Cheltuieli cu materiile prime şi materialeleconsumabile

b) Alte cheltuieli externe6. Cheltuieli cu personalul:a) Salarii şi indemnizaţii

b) Cheltuieli cu asigur ările sociale, cu indicareadistinctă a celor referitoare la pensii7. a) Ajustări de valoare privind imobilizărilecorporale şi imobilizările necorporale

b) Ajustări de valoare privind activele circulante, încazul în care acestea depăşesc suma ajustărilor devaloare care sunt normale în entitatea în cauză 8. Alte cheltuieli de exploatare Profitul pe anul financiar Profitul sau pierderea din exploatare9. Venituri din interese de participare, cu indicarea

distinctă a celor obţinute de la entităţile afiliate10. Venituri din alte investiţii şi împrumuturi care fac

parte din activele imobilizate, cu indicarea distinctă acelor obţinute de la entităţile afiliate11. Alte dobânzi de încasat şi venituri similare, cuindicarea distinctă a celor obţinute de la entităţileafiliate12. Ajustări de valoare privind imobilizările financiareşi investiţiile deţinute ca active circulante13. Dobânzi de plătit şi cheltuieli similare, cu indicareadistinctă a celor privind entităţile afiliateProfitul sau pierderea financiar(ă)

14. Profitul sau pierderea din activitatea curentă 15. Venituri extraordinare16. Cheltuieli extraordinare17. Profitul sau pierderea din activitatea extraordinar ă 18. Impozitul pe profit19. Alte impozite neprezentate la elementele de mai sus20. Profitul sau pierderea net(ă) a exerciţiului financiar

Transferul de rezerveDividendele plătite

Profitul reţinut în anul financiar

Table no. 2 Comparative structure of the profit and loss accountIn compliance with national laws (accounting

regulations consistent with European directives)In compliance with US GAAP standards

Turnover Cost of salesGross profitDistribution costsAdministrative expensesOther operating income (productive)Income from shares in group companiesIncome from other investments in fixed assetsOther income from interest and similar amountsInvested amounts written off Interest paid and other charges

Profit on ordinary activities before taxation

1 Net turnover 2. Changes in inventories of finished goods and work in progress3. Production made by the entity for its own purposesand capitalized4. Other operating income5. a) Raw materials and consumables

b) Other external costs6. Staff costs:

a) Salaries and grants b) Social security costs with a separate indication of

those relating to pensions7. a) Value adjustments in respect of tangible and

Tax on profit on ordinary activities

7/16/2019 studiu comparativ privind sistemele contabile

http://slidepdf.com/reader/full/studiu-comparativ-privind-sistemele-contabile 16/16

Analele Universităţ ii “Constantin Brâncuşi” din Târgu Jiu, Seria Economie, Nr. 2/2010

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 2/2010

148

Profit on ordinary activities after taxation

Extraordinary incomeExtraordinary profit

Tax on extraordinary profit

intangible assets b) Value adjustments in respect of current assets, to

the extent that they exceed the amount of valueadjustments which are normal in the undertakingconcerned

8. Other operating expenses Profit for the financial year Operating profit or loss9. Income from participating interests, with separateindication of that derived from affiliated undertakings10. Income from other investments and loans forming

part of the fixed assets, with a separate indication of that derived from affiliated undertakings11. Other interest receivable and similar income, witha separate indication of that derived from affiliatedundertakings12. Value adjustments of financial assets andinvestments held as current assets13. Interest payable and similar charges, with a

separate indication of that regarding affiliatedundertakingsFinancial profit or loss

14. Profit or loss on ordinary activities15. Extraordinary income16. Extraordinary expenses17. Profit or loss on extraordinary activities18. Tax on profit19. Other taxes not listed at the items above20. Net profit/loss of the financial year

Transfer of reservesDividends paidProfit retained in the financial year

Tabelul nr. 3 Conţinutul situaţiilor financiare în varianta românească şi varianta US GAAPConform legislaţiei naţionale (reglementărilorcontabile conforme cu directivele europene)

Conform normelor US GAAP

Bilanţ Cont de profit şi pierdereSituaţia fluxurilor de numerar Situaţia modificărilor capitalului propriu

Note explicative la situaţiile financiare anuale

Bilanţ Cont de profit şi pierdereSituaţia fluxurilor de trezorerieSituaţia modificării capitalului (sau Situaţia repartizării

profitului)Alte elemente

Table no. 3 Content of financial statements in the Romanian version and the US GAAP versionIn compliance with national laws (accounting

regulations consistent with European directives)In compliance with US GAAP standards

Balance sheetProfit and loss accountCash flow statementStatement of changes in equityExplanatory notes to the annual financial statements

Balance sheetProfit and loss accountTreasury cash flows statementEquity records (or Profit distribution statement)Other items