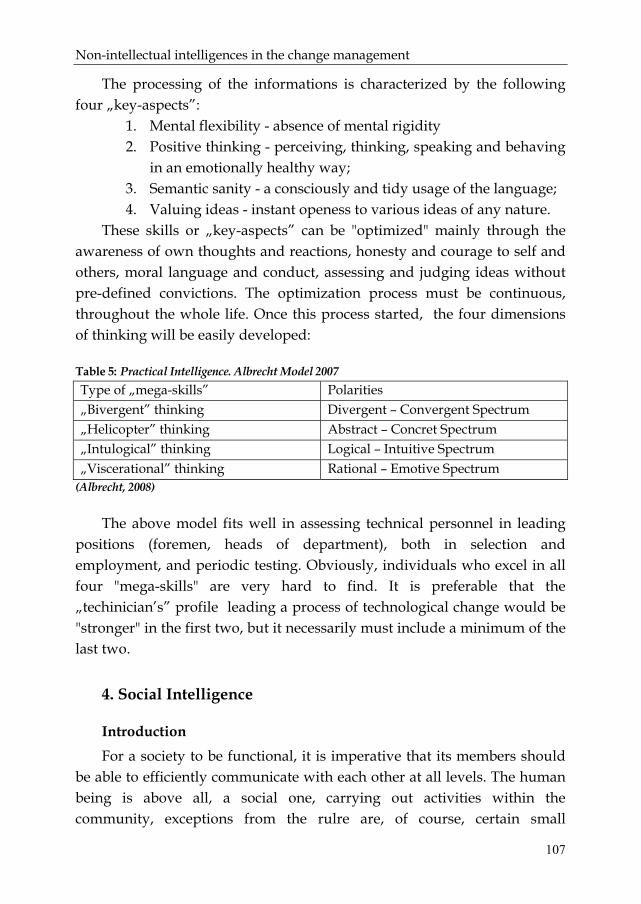

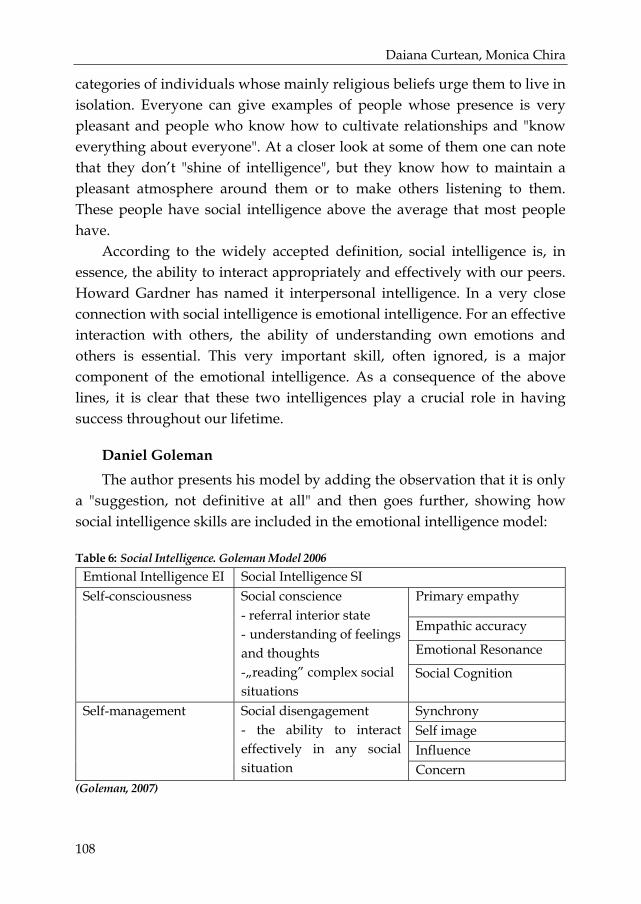

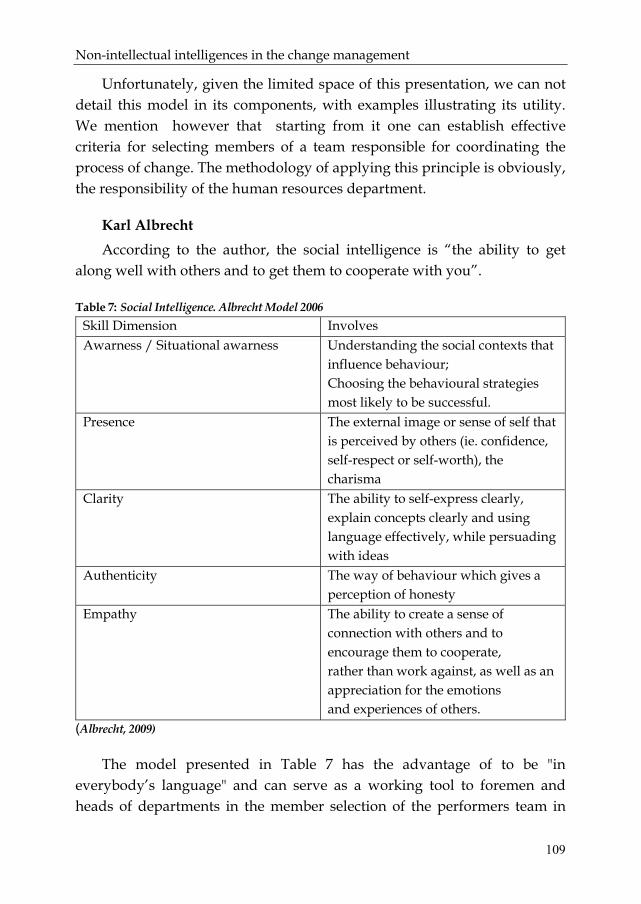

comitetul de coordonare - amazon s3s3.amazonaws.com/zanran_storage/extensii.ubbcluj... · german...

TRANSCRIPT

Comitetul de coordonare: Prof.univ.dr. Andrei Marga, Rectorul Universităţii “Babeş-Bolyai” Cluj-Napoca Prof.univ.dr. Pompei Cocean, Prorector al Universităţii “Babeş-Bolyai” Cluj-Napoca Conf.univ.dr. Cristina Ciumaş, Prorector al Universităţii “Babeş-Bolyai” Cluj-Napoca Prof.univ.dr. Ştefan Szamoskozi Prorector al Universităţii “Babeş-Bolyai” Cluj-Napoca Prof.univ.dr.Dănuţ Petrea Decanul Facultăţii de Geografie Prof.univ.dr. Dumitru Matiş Decanul Facultăţii de Ştiinţe Economice şi Gestiunea Afacerilor Prof.univ.dr. Călin Felezeu Decanul Facultăţii de Psihologie şi Ştiinţe ale Educaţiei Conf.univ.dr. Nicolae Boar Directorul Extensiunii Sighetu Marmaţiei Prof. Sandu Pocol, Prefectul Judeţului Maramureş Prof. Eugenia Godja, Primarul Municipiului Sighetu Marmaţiei

Comitetul de organizare: Conf.univ.dr. Nicolae Boar, E-mail: [email protected] Conf.univ.dr. Marin Ilieş, E-mail: [email protected] Conf.univ.dr. Gabriela Ilieş, E-mail: [email protected] Lect.univ.dr. Nela Şteliac, E-mail: [email protected] Lect.univ.dr. Mihai Hotea, E-mail: [email protected] Prof.asoc.drd. Viorel Dragoş, E-mail: [email protected]

Secretariat: Asist.univ.drd. Alina Simion, E-mail: [email protected] Asist.univ.drd. Diana Moisuc, E-mail: [email protected] Secretară: Iuliana Lihet, E-mail: [email protected] Secretar: Sorin Kosinszki, E-mail: [email protected] Referent: Alexandra Orza: E-mail: [email protected]

UNIVERSITATEA “BABEŞ-BOLYAI” CLUJ-NAPOCA

Facultatea de Ştiinţe Economice şi Gestiunea Afacerilor

EXTENSIUNEA SIGHETU MARMAŢIEI

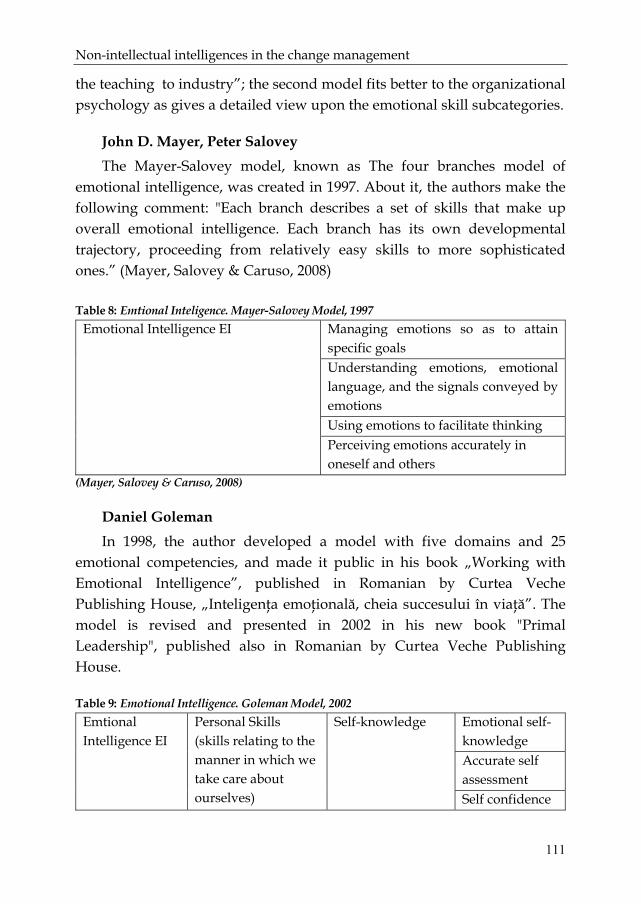

Conferinţa Internaţională

DEZVOLTARE ŞI INTEGRARE EUROPEANĂ

SECŢIUNEA B Dezvoltare economică în contextul integrării europene

SIGHETU MARMAŢIEI Maramureş-România 16-17 octombrie 2009

Manifestare ştiinţifică organizată sub egida “UBB 90”

Presa Universitară Clujeană 2010

ISSN 2069 – 024X

© 2010 Autorii volumului. Toate drepturile rezervate. Reproducerea integrală sau parţială a textului, prin orice mijloace, fără acordul autorilor, este interzisă şi se pedep-seşte conform legii. Universitatea Babeş-Bolyai Presa Universitară Clujeană Director: Codruţa Săcelean Str. Hasdeu nr. 51 400371 Cluj-Napoca, România Tel./fax: (+40)-264-597.401 E-mail: [email protected] http://www.editura.ubbcluj.ro/

5

Cuprins

Communication forms in the business / Avram Laurenţia Georgeta .... 8

The Local Development Strategy from the Economic Perspective – Evaluative Study for Cudalbi Commune, Galati Department / Florina Balcu...................................................................................... 17

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor din România / Florina Balcu .......................................... 31

The ethics of management of the non-reimbursable funds by the romanian SME’s / Diana Bălin, Aura-Mihaela Ioniţă .......... 43

Standardele Internaţionale de Raportare Financiară (IFRS) şi criza financiară / Boghean Cristina Iuliana ................................... 55

Analysis of the foreign direct investment (FDI) in Romania after EU accession / Braga Viorica, Mirea Gabriel ........................... 64

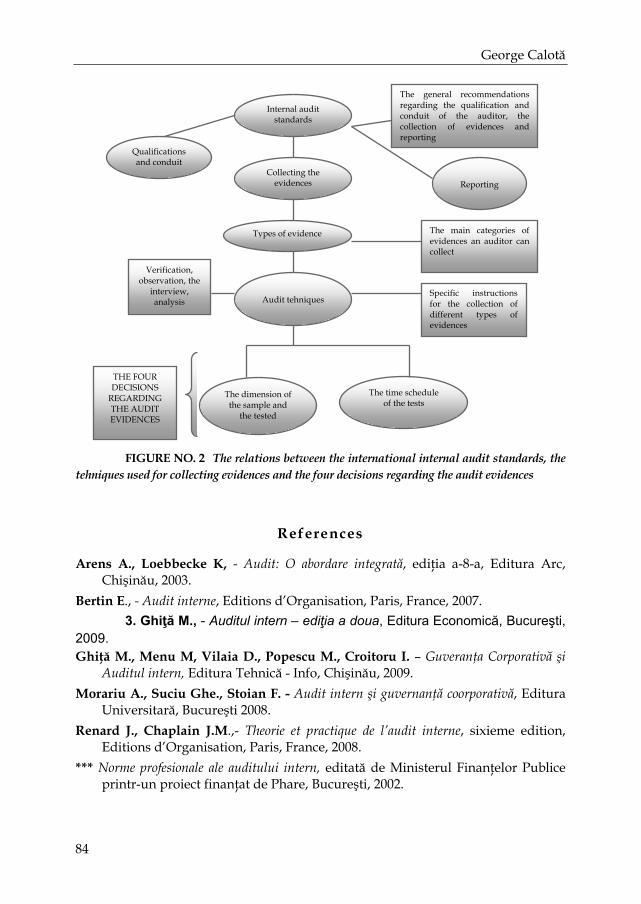

Audit evidences – Essential elements of the internal audit when respecting the international internal audit standards / George Calotă ........................................................................................ 74

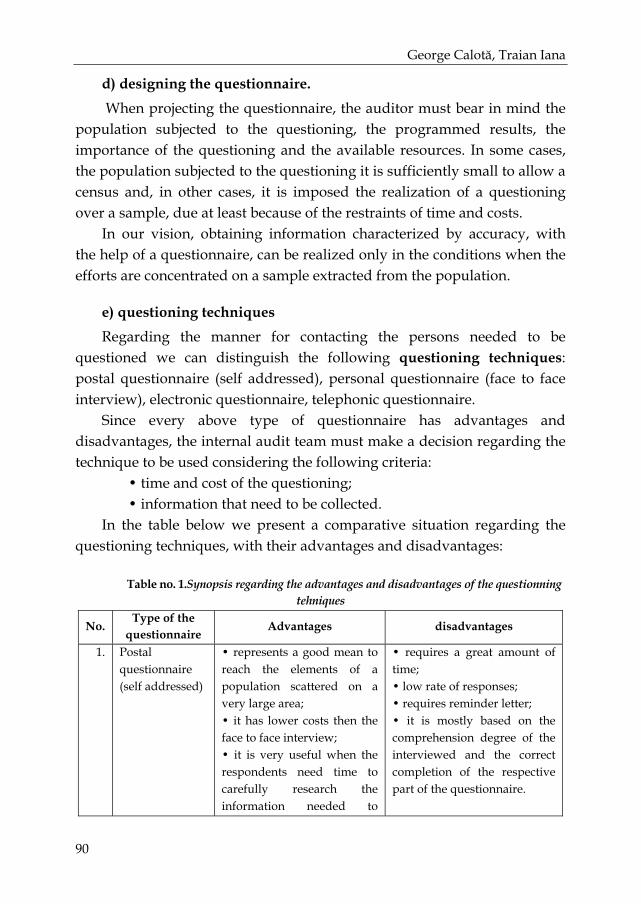

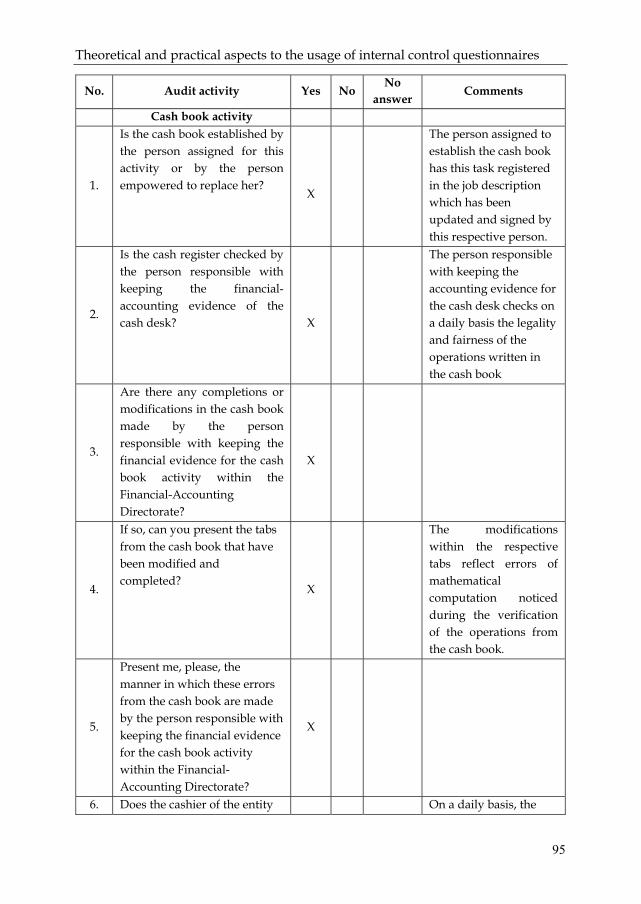

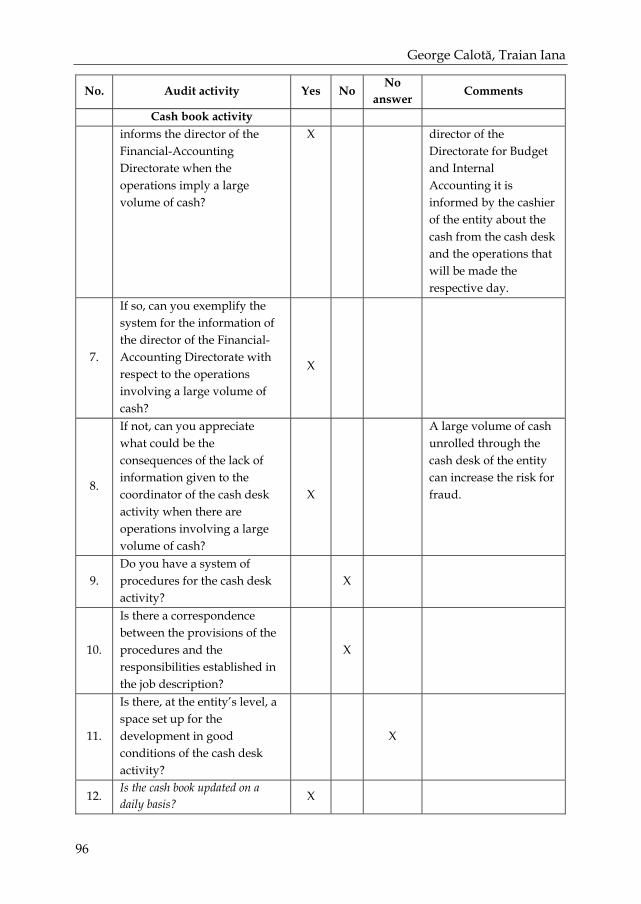

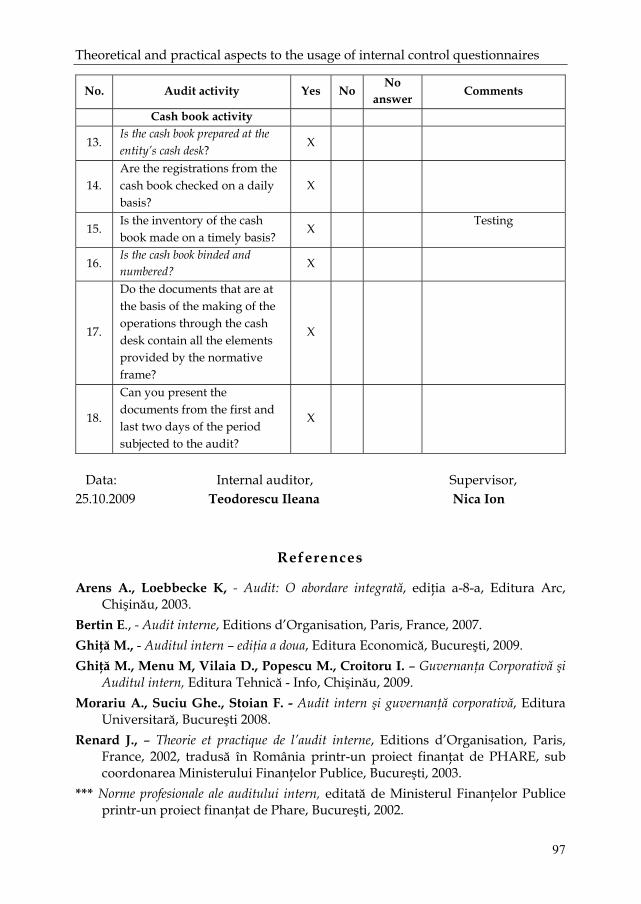

Theoretical and practical aspects to the usage of internal control questionnaires / George Calotă, Traian Iana ..................................... 86

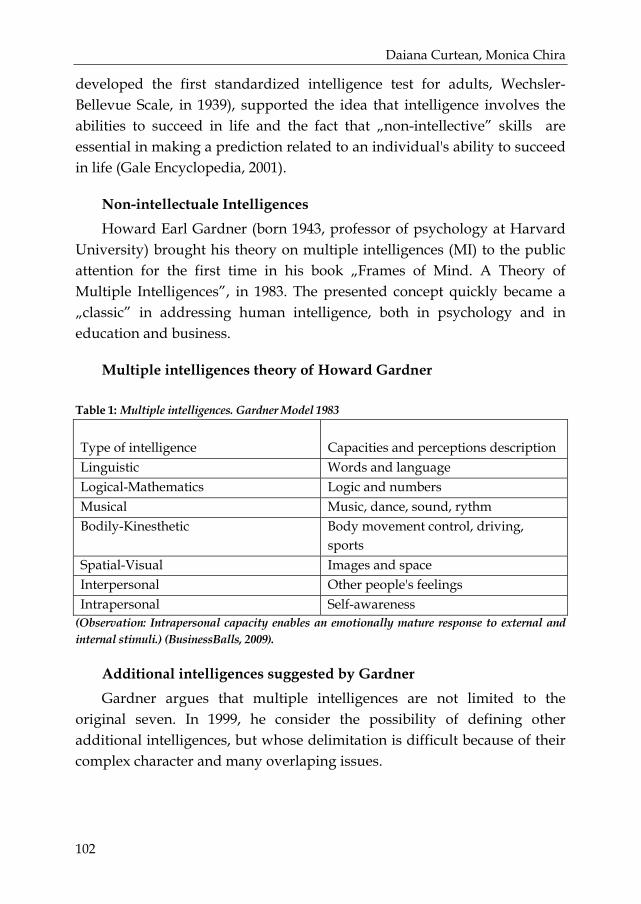

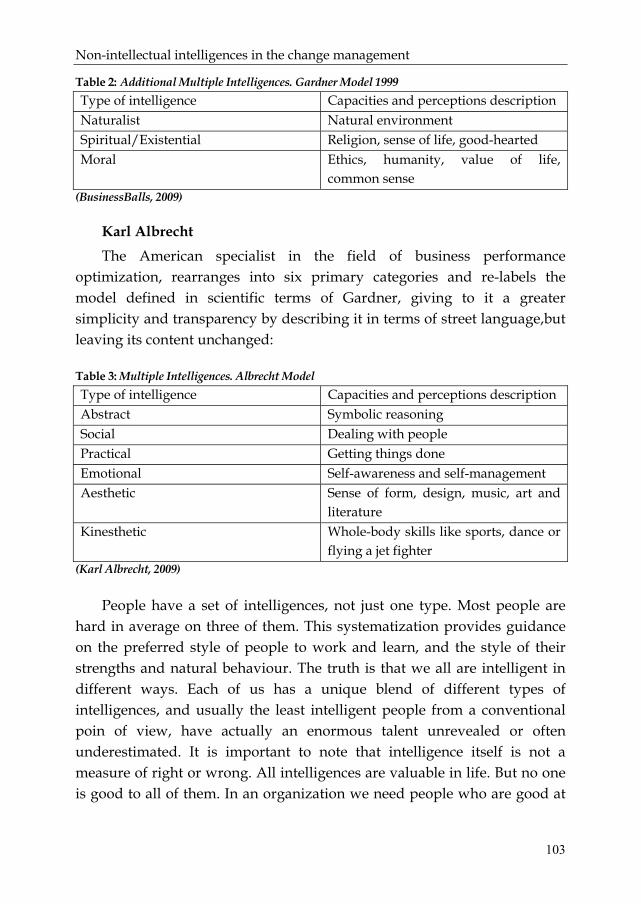

Non-intellectual intelligences in the change management / Daiana Curtean, Monica Chira ............................................................ 99

Short considerations regarding the Strategy for Sustainable Development at the EU and Romania’s level / Ionel Didea, Elise-Nicoleta Vâlcu ............................................................................ 114

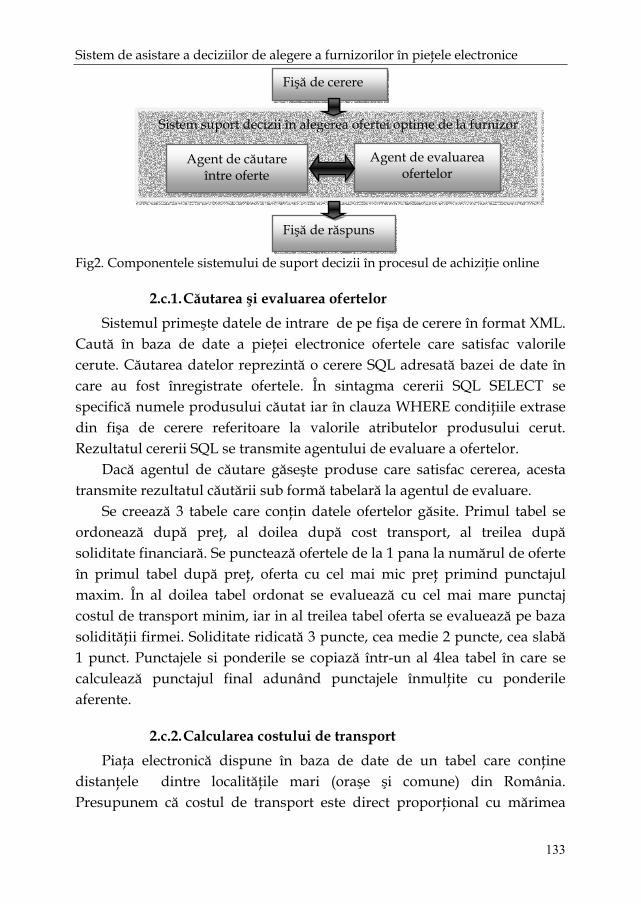

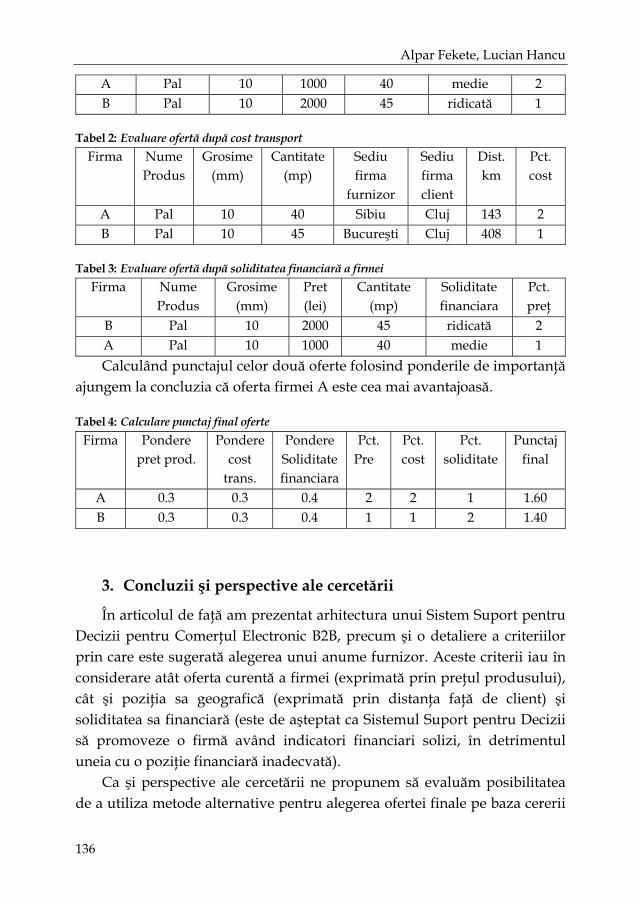

Sistem de asistare a deciziilor de alegere a furnizorilor în pieţele electronice / Alpar Fekete, Lucian Hâncu ........................................ 127

Fiscal Policy in Contemporary Financial Crisis / Mihaela Göndör ... 138

6

Fiscal Harmonization to further the goal of a single market / Mihaela Göndör................................................................................... 152

Equilibration and compensation of the risk structure in the german statutory health insurance / Grünewald Ioan B. ............. 167

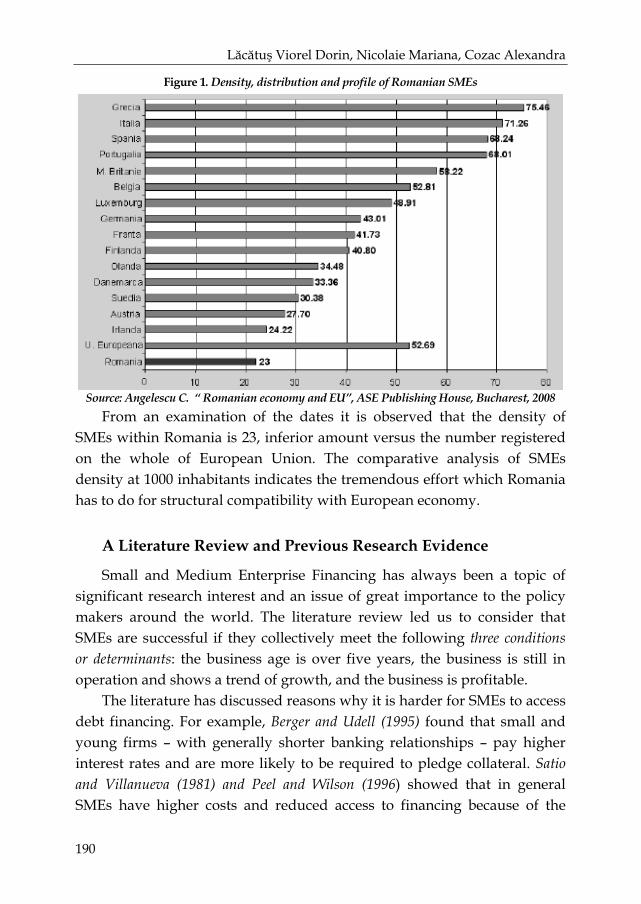

The regional development within the national economy / Romeo Ionescu..................................................................................... 179

Determinants concerning the access to financing romanian SME’s / Lăcătuş Viorel Dorin, Nicolaie Mariana, Cozac Alexandra............ 188

Studiul comparativ privind sistemul contabil anglo-saxon / Lenghel Radu....................................................................................... 199

Concepte teoretice privind taxa pe valoarea adăugata / Cristian Mazilu ................................................................................... 208

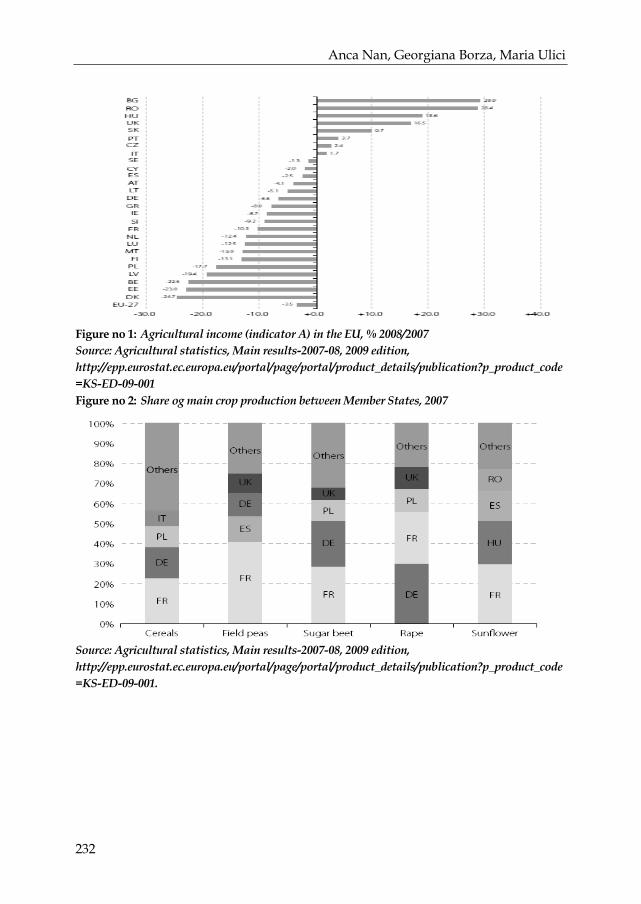

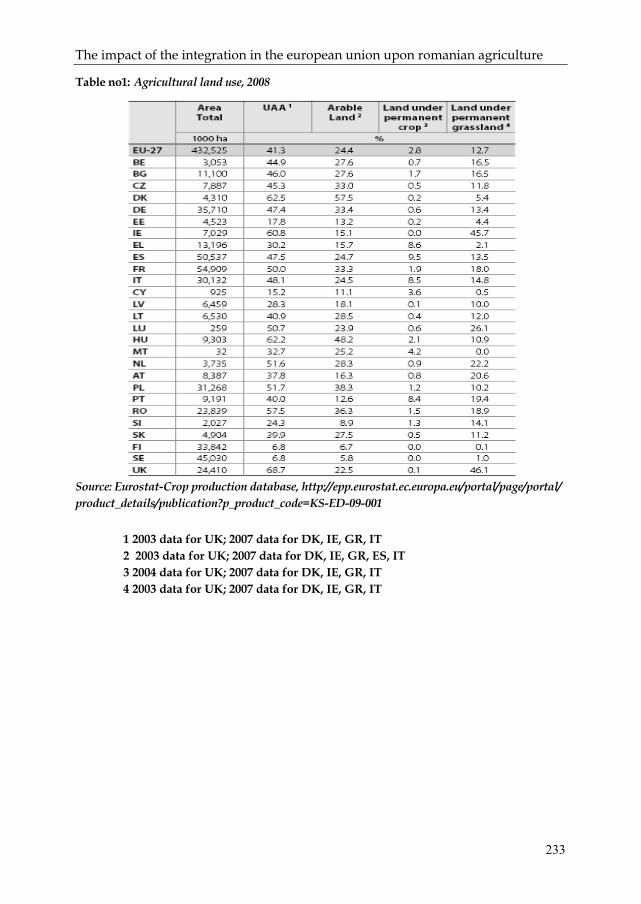

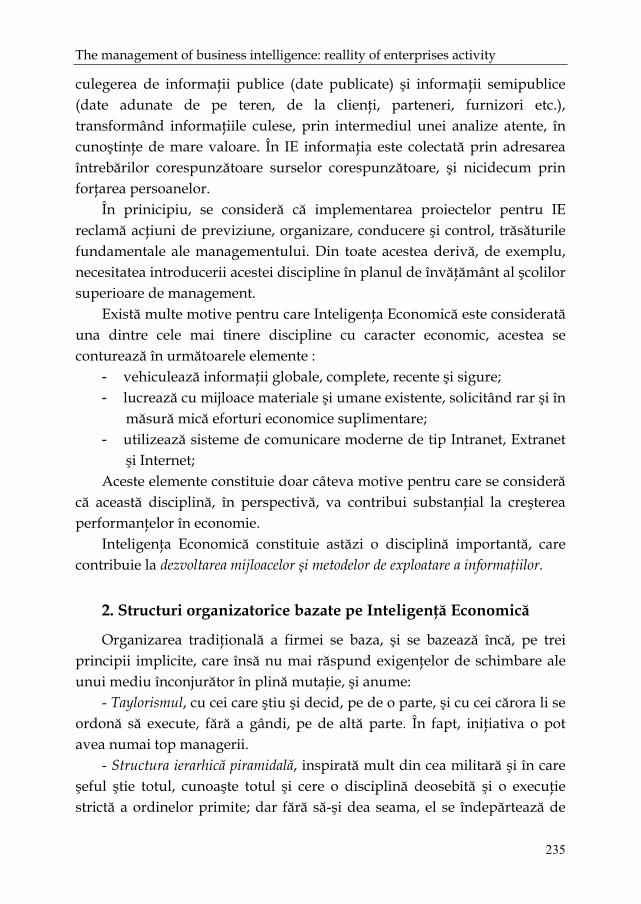

The impact of the integration in the european union upon romanian agriculture / Anca Nan, Georgiana Borza, Maria Ulici 215

The management of business intelligence: reallity of enterprises activity / Claudia – Mihaela Nicolau ................................................ 234

Starea actuală a business intelligence-ului la nivel internațional – literature review / Claudia – Mihaela Nicolau................................ 251

Human capital - investment and performance / Florentina Pantazi 267

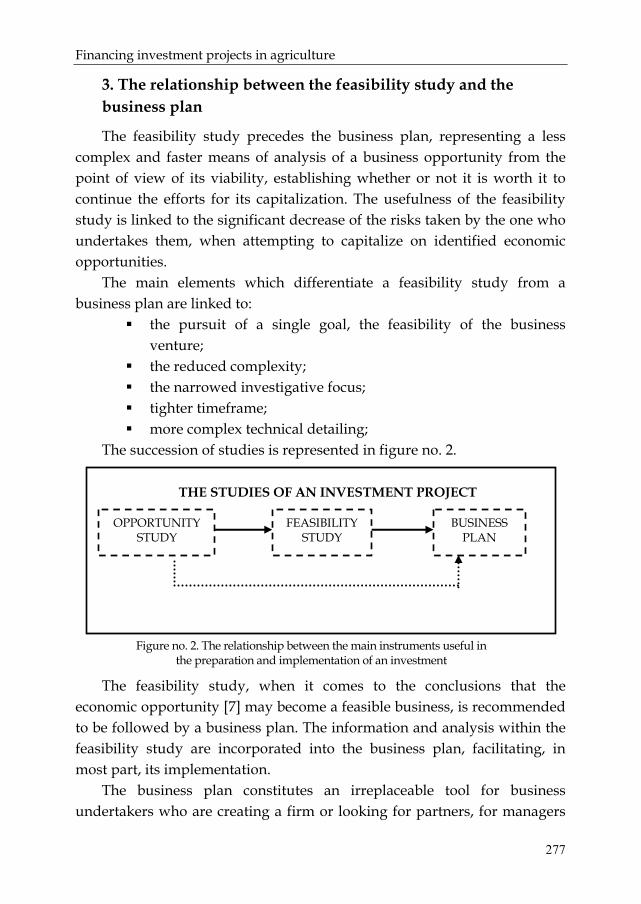

Financing investment projects in agriculture / Aurelia Oana Pârvulescu,Viorica Ioan, Alexandra Nicoleta Nicoară 271

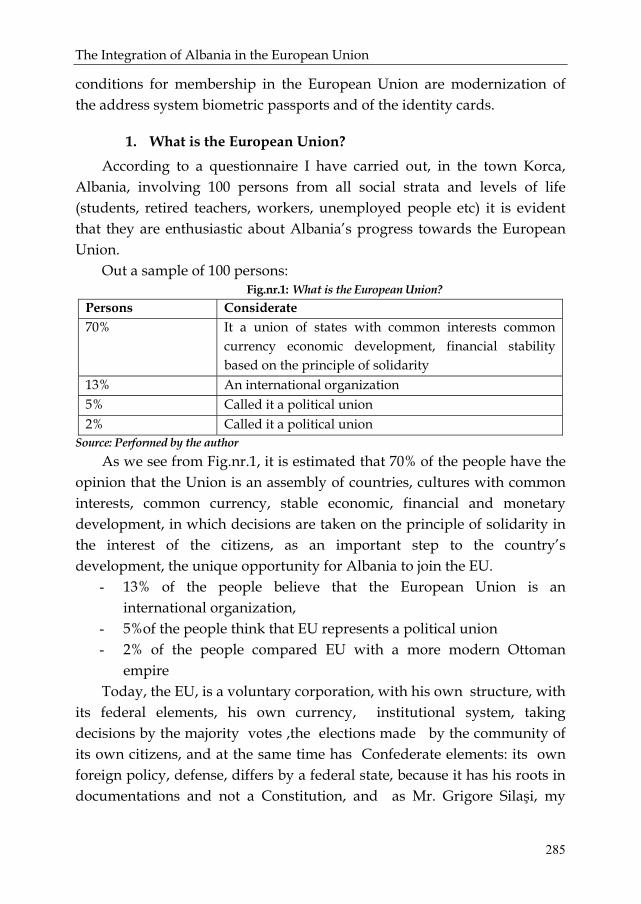

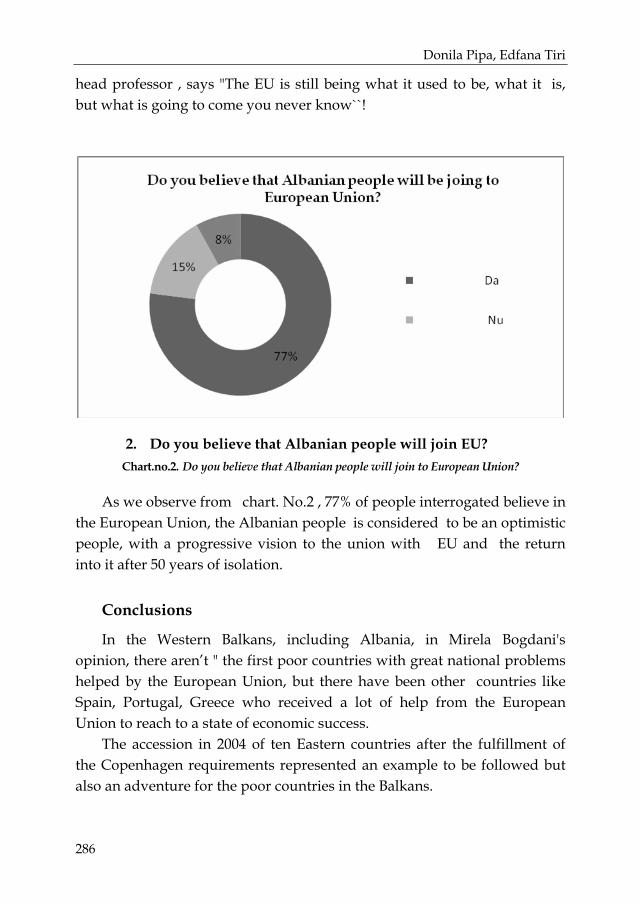

The Integration of Albania in the European Union / Donila Pipa, Edfana Tiri .......................................................................................... 283

Romanian linguistic integration into Europe / Ciprian-Viorel Pop, Adriana-Diana Polgar......................................................................... 288

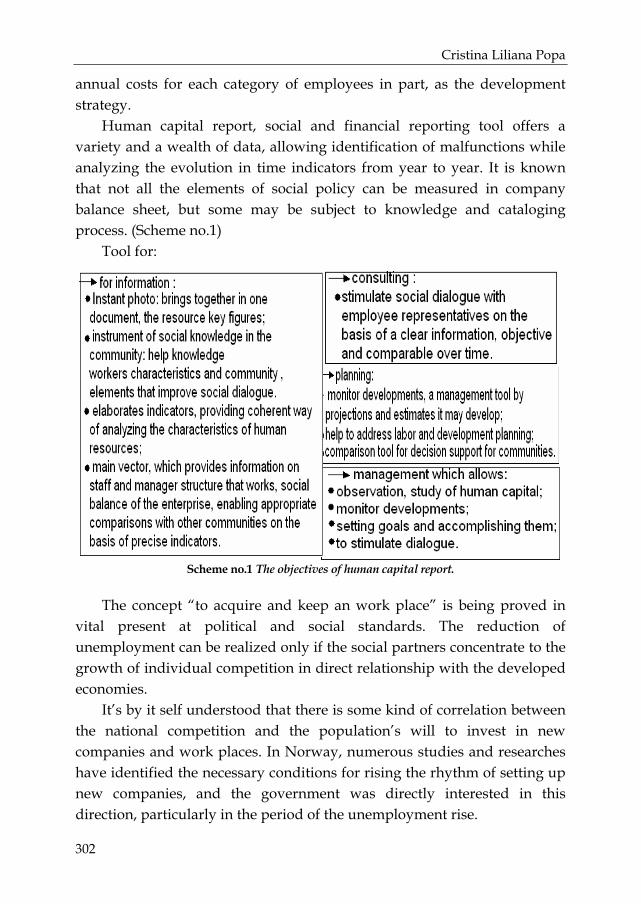

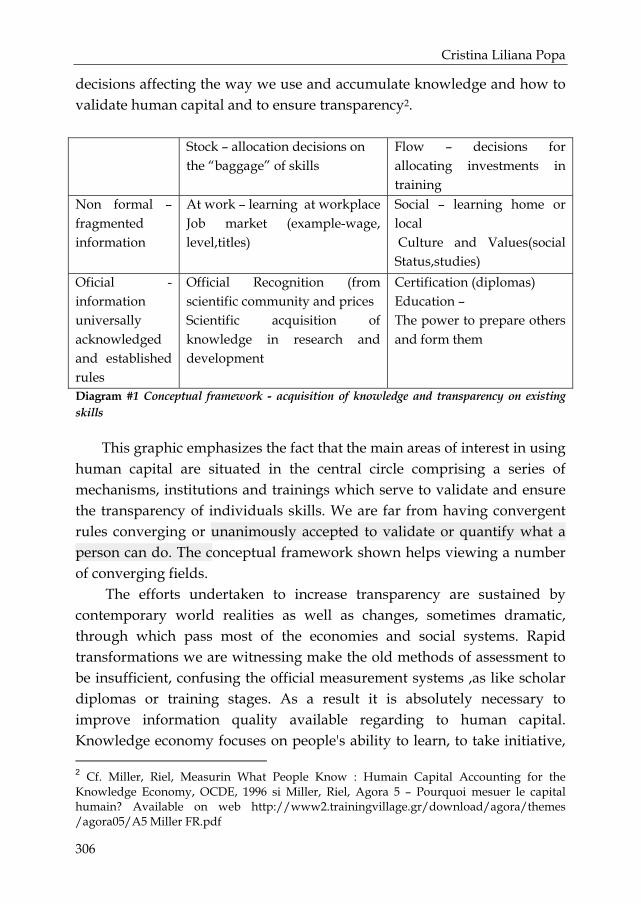

Achiving the human capital report, why and how / Cristina Liliana Popa .......................................................................... 300

Imf’s and governments’ support to financial system in the european countries during the crisis / Magdalena Rădulescu ..... 309

7

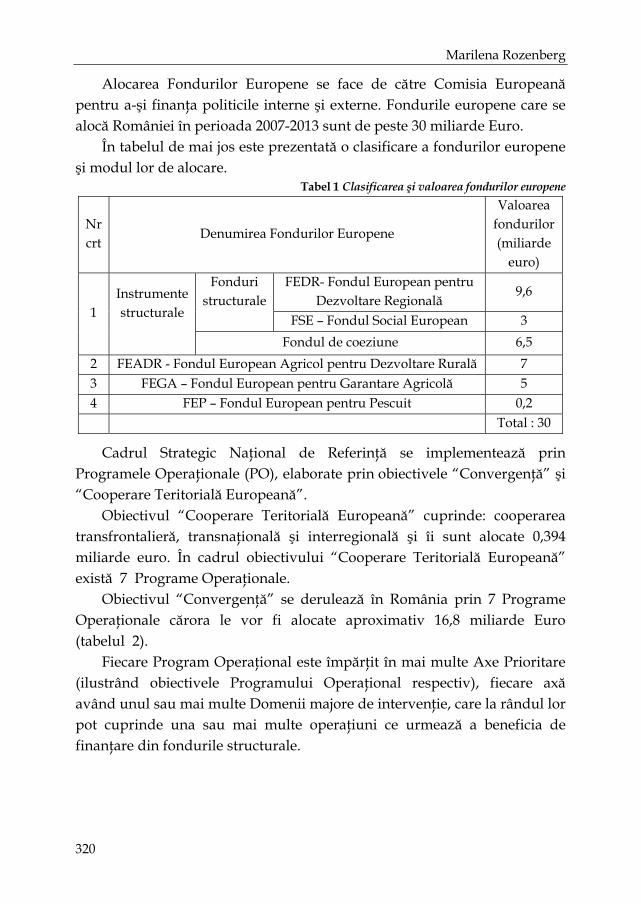

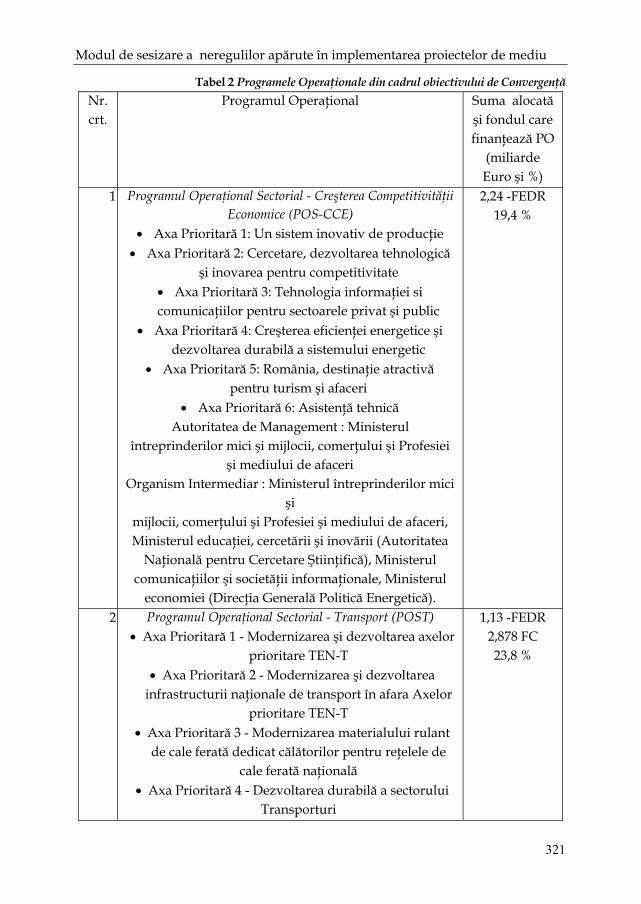

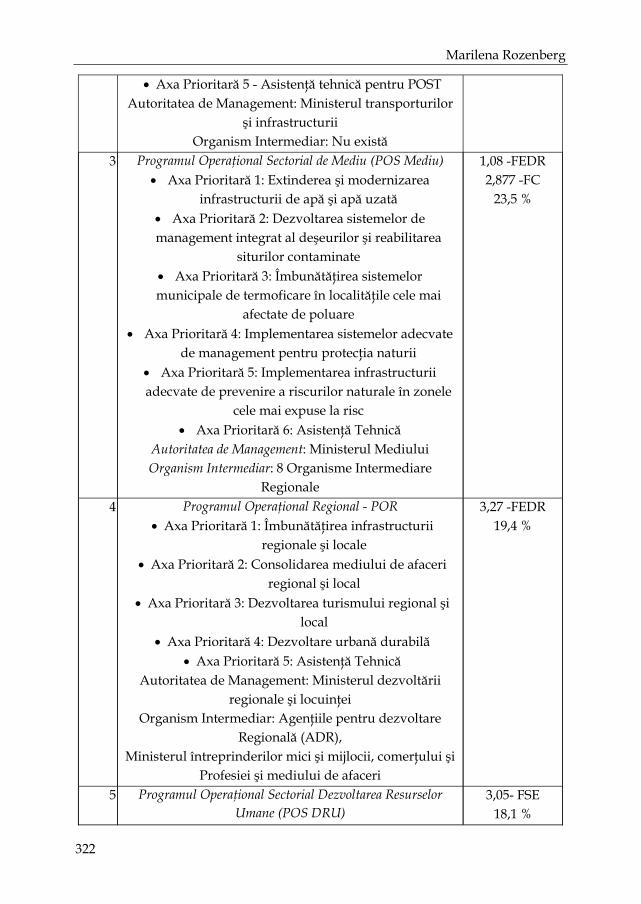

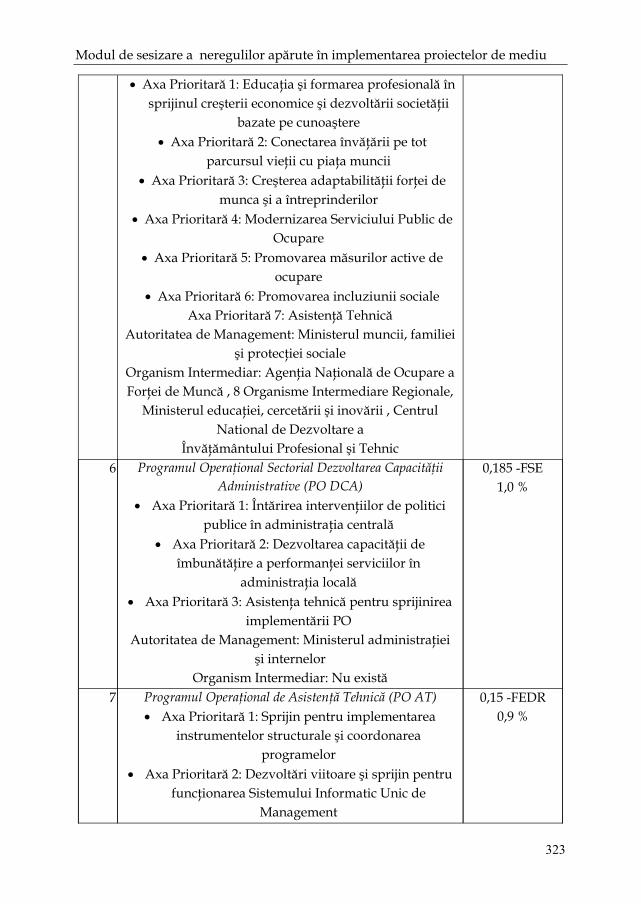

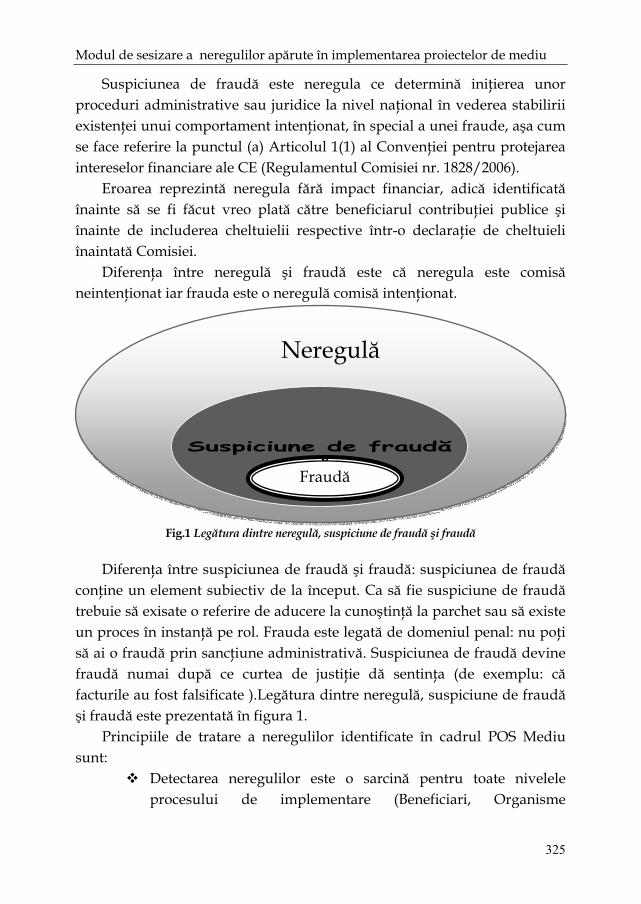

Modul de sesizare a neregulilor apărute în implementarea proiectelor de mediu finanţate din fonduri europene / Marilena Rozenberg ............................................................................ 319

Considerations upon the role of the emotional intelligence in the human resources management in tourism / Andreea Măriuca Rus, Daiana Curtean ............................................. 330

Particularities of fixed assets. Accounting and fiscal treatment / Laura Sărac Aldea ............................................................................... 344

Diagnosis of managerial competence trough the professiogram method – comparative study according to the enterprise size / Anamaria Tohătan ........................................................................... 378

Regions and "shared governance" at the eu level in the context of the current economic crisis / Elise-Nicoleta Valcu, Ionel Didea ... 389

The role of the profit and loss accounting information / Odi Mihaela Zărnescu ........................................................................ 398

8

Communication forms in the business

Avram Laurenţia Georgeta*

The business human activity takes place in the middle of a universe of communication. In the designing of a business and in the everyday presumed steps are necessary real and conclusive information, past and present about the national and international economic field and about the consumer and competitor etc.

The business man success depends, therefore, by his ability to select the essential information, to penetrate the rich information flows, concentrated, polyvalent. The explosion of information, its complexity requires to receiver the access to the main content of messages.

Information is considered, along with raw materials and energy, one of the fundamental resources of the society. Information is constitutive for the company and socially, the communication is essentially, being an information transfer. The communication needs of the social persons occur in each of their actions and the information universe, space and time, retrospectively and prospectively and make their whole experience. Based on this experience, the businessmen are able to distinguish between essential and superfluous, current and outdated, truth and error.

The business managers do not treat information as the disparate elements, but as parts of the information system underlying the adoption of decisions.

Communication is what allows any "full" to work. "All" can be an individual, one team, one community, one nation, a conglomerate of nations and a global population. From this perspective we can conclude that those who are master in communication to the level of art, can become "winners" - in that may look with confidence to the future and may be those who show so continuously succeed. In the mentality and in the logic of abundance we are continuously "winners" and can, at any moment, to freely choose a "proper interpretation of events" - which can be viewed as successes (and for any harm that pays well - as said the proverb).

* Nedeclarat

Communication forms in the business

9

The holistic communication (total) and awareness of sequence of increasingly large in the way it allows the success in any activity or area to acquire new meanings. In recent years, the successful interdisciplinary collective brought new evidence in support of "possible decoding of information from the living world" more able to expand the horizon of human knowledge.

The complexity theory and the studies based on allowed the awareness of multiple levels of understanding and application of communication elements. Much old information is re-evaluated, receives new meanings and forms the basis for new techniques and methods of communication. A special emphasis is placed on the ethics of communicating, the fundamental principles of harmonious living.

Today, we can confidently use creative techniques, intuitive, logical, creative imagination over time. Implementing in the communication could open new horizons, could allow the development of latent abilities.

Communication is an essential link in the normal operation of any system. The ecological systems of communication are a real art. The art of human communication is as old as the world and is constantly growing. There are three major sequences:

• The non - verbal communication; • The verbal communication; • The holistic communication. Each of them has come through the stages of awareness or, in the sense

that although everything is in everything (as holistic theory of the universe) each generation of creatures chooses, according to the natural laws, to use a specific sequence of more or less of communication holistic.

In fact, any living organism communicates holistically - but realizes only a part of communication. Some creatures - humans, for example - have the ability to voluntarily activate more extensive sequences of holistic communication.

Human civilization is a brink of a leap in the level and depth of communication. In addition to the biological aspects of communication we assist at the development of its technical aspects. We can already say that the third millennium is a millennium of the holistic communication. The first phases include:

Avram Laurenţia Georgeta

10

• Development of the capacity to use increased quantities of information;

• Development of the logistics base (natural or artificial) for efficient use of information;

• Development of the native database of the information holistic processing;

• Development of the holistic science communication; • Development of the Millennium 3 informational civilization. The experts forecast an unprecedented development of human culture -

based on the quantity and the quality of information used in exceptional harmonious systems. It may foreshadow four stages:

• Development of the individual applications, based on “personal diary - in different versions”

• Development of the family application; • Development the applications in the groups of friends; • Development the complex community application. There are expected in the near future, significant developments in the

fields: • Formal aspects of the holistic communication; • Complementary aspects of communication (actions with

informational purposes); • Unconventional aspects of the harmonious communication in the

nature; • Bio-chemical issues and information in the near future of

communications. So, it is hard to believe that a successful business is possible without

effective communication between all involved in carrying them. The communication needs of the social persons occur in each of their

actions, the communication is constitutive of the human nature. “Man is, above of all, language”1, the philosopher Karl R. Popper said, referring to the verbal language.

1 Popper, K.R., Viitorul este deschis, Editura Trei, Bucharest, 1997, p. 124

Communication forms in the business

11

Interest for the art of communication occurred since antiquity2, the Greeks are those who, by developing methods and techniques of communication, gave him the status of science. In the contemporary period, the communication theory knows an impressive development, being the source of the concern for many different professionals: psychology, philosophy, marketing and management etc.

To the communication concept, it was awarded, over the time, many different understanding. In the speciality literature, the exact meaning of the concept is still alive and discussed, the perspective approach and significance attached to the concept being different. In the view of Dance, F.3, the communication is the process of transmitting a message through a channel to a receiver of information. To define the communication as an exchange of messages between an issuer and receiver is a simple reflection of the essence of this process.

The communication process is irreversible and can be analyzed on four separate levels: intrapersonal communication, interpersonal communication, group or organizational communication, mass communication. From the perspective of our research, we are interested by two of the forms namely:

• Interpersonal communication, direct or intermediate, held between individuals (managers, employees, associates, business partners).

• Communication in the organizational structures (the business communication).

On a business level we talk about the formal, official communication carried by hierarchical channels and informal communication, held outside the official channels.

Whatever is the form and the flows that is achieved, the communication tends to influence or change perceptions, attitudes, behaviors, feelings, opinions of an individual or a group of individuals.

Unprecedented expansion of science and technology knowledge in a knowledge society, the further development of the new information

2 Human communication theory flourished in Athens, where he met a large field of development. The science and the art to communicate convincingly were called rhetoric and was the subject of study in the Athenian universities. 3 Dance, F.E.X., The Concept of Communication, in ,,The Journal of Communication’’, No. 20 Landon

Avram Laurenţia Georgeta

12

technologies and enhance the volume of information necessary for proper business operations have resulted in an impressive diversification of forms of communication.

Besides the classical forms of communication (written, verbal and nonverbal), appeared interactive communication based on the virtual techniques of communication, networks of computers, telecommunications equipment, etc. It provides, at present, the dynamic solutions of communication that enable the development of business relationships through collaboration and coordination of all participants, regardless of the geographical area where they are. Each form of communication which is called in business practice has specific advantages and disadvantages which need to be considered in the design and operationally of an effective system of communication4.

The written communication has the advantage that the message can be prepared more carefully and with consideration of procedures and actions partner relationships. The written texts can be archived, making it possible to be read and refer to them at any time. Effectiveness of written communication depends by the content of the written message which must be expressed concisely, clearly, logically and directly. The disadvantage of this form of communication is appearance of misunderstanding situations at the receiver, of the meaning of the message was designed by the issuer, and missing an immediate response from the receiver.

The oral communication is done directly between partners and allows the rapid exchange of information. It offers an immediate response and clarify any disagreements.

The nonverbal communication is part of the visual record of the service and usually accompanies the verbal messages. There is manifested like a body language form (position, gestures, mimicry) or a par verbal language (voice, tone and pace of speech). Its effectiveness lies in the match with the verbal messages and completing the content of it. Science has shown that nonverbal communication is important how we transmit information, sometimes more important than what we deliver. Although this fact is often overlooked, the business people must not forget that the “posture,

4 Camelia Ştefănecsu, Managementul afacerilor, Editura Fundaţiei România de Mâine, Bucharest, 2008, p. 80

Communication forms in the business

13

movements, gestures and gaze are relevant of the confidence that you have in yourself and the relationship you want to establish a receiver”5.

The electronic communication develops concepts and new attitudes in the business, a different way of dealing with relationships, installing a new philosophy of communication in the businesses. Based on the modern information technologies, it speeds up the progress of the business through rapid access to information and increased opportunities for global communication. The global communication is a relatively new concept, which experts give special significance is presented as a “combination of two techniques: advertising and public relations” or as a “meeting of more specialized companies, each in a communication discipline, animated by a central coordinator”6.

The radical transformation produced by the development of the information and communications technology have created serious mutations in the business practice, opening new opportunities to modernize the ways of communication and broad access to information of those who operate in this area. The new information society evolves rapidly, forcing firms to adapt to the new communication technologies to benefit from the convenience of them and to evaluate effectively, the business opportunities. At the base of the electronic communication is the computer through which the receiving, storing and processing information in digital form, to be transferred anywhere in the world via internet.

The tough competition and the large amount of information flow, the necessity of the rapidly response to the changes produced by the global market have led to the spectacular developments of the electronic communication channels in business. This expansion was supported by the Internet. Referring to the implications of the Internet on the business development, Bill Gates7 claimed that, soon, the most of the information to be transmitted by digital, the conditions under which business will be connected to the Internet, administrative processes, which now is done on

5 Arcad R., Boureanu, N., La Communication Efficace. De l’intention aux mozens d’expression, De Boeck Universite, Bruxelles, 1998, p. 314 6 Cathelat, B., Styles de Vie, Les Edition d’Organisation, Paris, 1985, p.6 7 Gates B., Afaceri cu viteza gândului. Spre un sistem nervos digital, Editura Amaltea, Bucharest, 2000, p. 72

Avram Laurenţia Georgeta

14

hard paper, will be replaced in future with digital processes and the e-mail will become common.

Behold, a few years after that prediction, the reality of the business practice claims by Gates were confirmed, at present, the electronic communication is widely used in business relations. Furthermore, the implementation processes and the problem-solving assistance with the computer and obtaining new generation of computer applications have revolutionized the communication system in the business practice.

In the business management, the interactive communication based on new technology, has an extra dimension. It facilitates contacts and cooperation with current and potential partners and drive forward the development of new channels of cooperation between people who have common interests: identifying customers and their needs is made easier, information about business partners are more accessible, customer requests are received fast, etc. However, this form of communication enables companies, to better understand the competitive challenges through an integrated flow of information directed exactly where it needs exactly the right time within an organization8.

The interactive communication system stimulates and makes business processes and organization relations in all sections, regardless of the time and space. One example is the use of Internet facilities provided for information and communication messages. With the diversification of methods of the global communication, through extending the Internet access has been a revolution in the business. Now any company can make a web page creating software that describes the products and services they performed. Large companies are building their sites complex, structured information, giving consumers worldwide data on specific activities and products what it offers, and other services whose share is growing.

Experts9 report the emergence of a new concept, that of the electronic business. This concept envisages a new approach to the economic transactions, aimed at developing on-line for all stages of a business:

8 Gates B., Afaceri cu viteza gândului. Spre un sistem nervos digital, Editura Amaltea, Bucharest, 2000, p.11 9 Ivan I., Economia digitală şi societatea informaţională, în Dezvoltarea durabilă a României şi Republicii Moldova în contextul european şi mondial, Editura Expert, Bucharest, 2006, p. 351

Communication forms in the business

15

presentation of the offer, negotiation, documentation, contracting, payments and receipts.

“Now everybody stands in front of the computer, anyone can publish anything about what others do” said Joseph Ghossoub, president of the International Advertising Association at the IAA European Summit held in September 2007, highlighting the risks to which corporations are exposed in the absence of the appropriate rules in this area. Security and privacy are assured with difficulty. The business ideas, the confidential information may be stolen by “attacks” on the networks of computers10.

None of the forms of communication presented is perfect. Option for the most appropriate method of communication in a certain time, in business practice is based on the various factors: The main objective of communication, target audiences, expected impact, cost of communication, understanding, degree of selectivity degree of credibility, etc. Regardless, however, of many forms and channels of communication, their effectiveness is conditional on how they are used, realized and, if possible, controlled.

Bibliography

Arcad R., Boureanu, N., La Communication Efficace. De l’intention aux mozens d’expression, De Boeck Universite, Bruxelles, 1998

Big Radu, Mircea Lobonţiu, Radu Coteţiu: Inovarea – Sursă de Dezvoltare Antreprenorială, Editura Limes, 2007

Camelia Ştefănescu, Managementul afacerilor, Ed. Fundaţiei România de Mâine, Bucharest, 2008

Cathelat, B., Styles de Vie, Les Edition d’Organisation, Paris, 1985

Dan Popescu, Conducerea afacerilor, Ed. Gil, Bucharest, 2001

Drucker Peter F., Societatea post-capitalistă. Ed. Image, Bucharest, 1999

Elaine Sternberg, Just Business. Business Ethics in Action, 1994

Fraisse H. , Manuel de l’ingenieur d’affaires, Editions Dunod, Paris, 1990

Fukuyama Francis, Marea ruptură natura umană şi refacerea ordinii sociale, Ed. Humanitas, Bucharest, 2002

Gates B., Afaceri cu viteza gândului. Spre un sistem nervos digital, Editura Amaltea, Bucharest, 2000

10 Morozan C., Comunicarae interactivă bazată pe tehnologie. Influenţe asupra afcaerilor, in publihing Marketing-Managemnet, no.5, Bucharest, 2006, p. 97

Avram Laurenţia Georgeta

16

Giordan, A.E., Expotrer plus2, Editions Economica, Paris 1998,

Godin.S, Conly C., Businss Rules of Thumb, Warner Books, 1987

Igor Ansoff, Implanting Strategic Management, New Jersey, Pretince-Hall, 1984

Ivan I., Economia digitală şi societatea informaţională, în Dezvoltarea durabilă a României şi Republicii Moldova în contextul european şi mondial, Editura Expert, Bucharest, 2006

Mihalciuc M., L.Mureşan, G.Stanciulescu, S.Stan,L.Csaba, Dictionar poliglot explicativ (româna, engleza, franceza, germana, maghiara, Editura Enciclopedică, Bucharest, 1996

Morozan C., Comunicarae interactivă bazată pe tehnologie. Influenţe asupra afcaerilor, în revista Marketing-Managemnet, nr.5, Bucharest, 2006

Nash Laura , Good Intentions Aside. A Manager’s Guide to Resolving Ethical Problems , 1993

Pâinişoară, I., Comunicarea eficientă, ediţia a II-a, Editura Polirom, Iaşi, 2004

Popescu Dan, Conducerea afacerilor, Ed. Gil, Bucharest, 2001

Popper, K.R., Viitorul este deschis, Editura Trei, Bucharest, 1997

Russu Corneliu, Management strategic, Editura All Beck, Bucharest, 1999

Corneliu Russu, Management, Edit. Expert, Bucharest, 1993

Toia Adrian, Noua Economie- Probleme economice, sociale, ştiinţifice şi tehnologice, in vol. Economia 2000, ed. ASE, Bucharest,

xxx- Annual Report on Corporate Governance 2004 – Corporate Governance recommendations, OECD

xxx- OECD Guidelines for Multinational Enterprises and Other Global Instruments for Corporate Responsibility, June 2001

xxx- GREEN PAPER – Promoting a European Framework for Corporate Social Responsibility

xxx- Dance, F.E.X., The Concept of Communication, in ,,The Journal of Communication’’, NR. 20 Landon

xxx- www.eu.int

xxx- www.orse.org

xxx- www.ilo.org

xxx- www.infoeuropa.ro

xxx- www.praward.ro/resurse-pr

17

The Local Development Strategy from the Economic Perspective – Evaluative Study for Cudalbi Commune,

Galati Department1

Florina Balcu*

Abstract: In the context of the local development, the development strategy during 2008

– 2018 for Cudalbi commune is a useful working instrument for the Cudalbi Local Council, representing the appropriate approach for the elaboration of some documents of reference necessary to access European funds. The purpose of the elaboration of strategy was to determine the directions of development, to make efficient the activity of the public authorities, to promote the town and to attract the financing sources in order to put into practice the planned projects.

JEL Classification: O12, O18 Key words: strategy, local development, economic analysis

1. Introduction

The economic activity of Cudalbi commune is centred upon agriculture. One of the general aims of the local policy, meaning the development of agriculture, is convergent to the objectives of the regional policy of the South-East Development Region.2

Although the industry is well represented, agriculture is a very important field for the economy of the region: about 40% of the employed population work in this field, which contributes with 16% to the regional Gross Domestic Product (GDP). The cultivated land occupies 65% of the

1 The work represents a part of the author’s research activity, as a member of project team led by conf.univ.dr. Puşcaşu Violeta within the contract no. 7955/2008 financed by the Local Council and Cudalbi Commune Hall, Galaţi Department * Facultaty of Economic Sciences, adress: 59-61, Nicolae Bălcescu Street, Galaţi, e-mail: [email protected] 2 Puşcaşu Violeta, Chiriţă Viorel, Balcu Florina, Răducan Oprea, Şorcaru Iulian, Strategy of Local Development –Cudalbi Commune: potenţial and perspectives, Europlus, Galaţi, 2008, p. 137

Florina Balcu

18

surface area and has a great potential of development in the future. Although there is agricultural potential, the capacity of processing the agricultural products is limited because of the old technologies. The high degree of fragmentation of cultivated land is another obstacle for agricultural development. The low economic potential of small farms and their inefficient management also determined the under-development of the processing of agricultural products.

In 2006, the South-East region ranked first nationally concerning the production of specific products, namely grape and sunflower production, and second for the wheat, grains and beans production. In terms of the livestock and animal husbandry sector, the region ranks first for mutton and goat meat production as well as for wool production, while the contribution of the village is well below.

The evolution of the main economic indicators in the region is presented in appendix 1, on categories, following the main indicators such as: population, employment, unemployment (total population, employed population, unemployment rate); economic development (GDP, FDI3, SME- small and medium sized enterprises); infrastructure (transport, public utilities, education, health services, social and touristic services).

The regional GDP (2.661,35 euro per capita) is close in value to the country GDP (2.932,86 euro per capita), but at the level of Galati county, it represents 2.542,81 euro per capita. Among all the parts of the region, Galati County ranks second, after Constanta County with the GDP value of 3.640,82 euros per capita.

The general trend must be of GDP growth at the level of Galati County, a growth that implicitly would determine a better living standard for the community.

The sector of small and medium sized enterprises is also well represented, at the SMEs indicator for 1000 inhabitants, because the country average is 20, 38 SMEs and the South-East Region has 18,63 SMEs per thousand inhabitants. Moreover, of the total 440,714 SMEs registered in 2006, 53,021 are related to south-east region, which means a share of only 12% of the total on country.

3 Foreign direct investment

Evaluative Study for Cudalbi Commune, Galati Department

19

Comparing the lines of industry we notice that the service sector in the most developed, with a share of 82, 57%, even exceeding the national average (79,53%).

Taking into account the SMEs size, most of them are microenterprises, namely companies with up to 9 persons.

It is well known that, for the economy, the SMEs sector brings the main sources of income to the national budget that is why we consider that boosting their development is a factor of interest both locally, regionally and nationally.

Taking into account the development of the region we belong to and also the actual economic context of economic globalization, we can approach the aspects concerning local economy, namely at the level of Cudalbi Commune.

The development strategy at the level of a local community must be integrated in its department and region evolution, following the national strategic development plan according to the specific features of the region.

2. Economic analysis of the private sector at the level of Cudalbi Commune

Considering data delivered by the Trade Register Office of Galati Court, subordinated to the Ministry of Justice, the situation of the companies as well of some other types of legal organization, including the working points created at the level of Cudalbi commune since 1991, we submit table no.1.

The analysis of legal person’s situation for the period 1991-2008 was performed for all the existent forms of incorporation, namely:

- registered sole traders (individual service providers); - family business; - family enterprises ; - individual enterprises ; - limited liability companies (LLC); - joint-stock companies; - partnership firms; - cooperative organizations.

Table no. 1 Companies situation in the Cudalbi commune

Florina Balcu

20

Companies Totalul societăţilor înfiinţate (1991-2008)

Total defunct

companies

Defunct companies

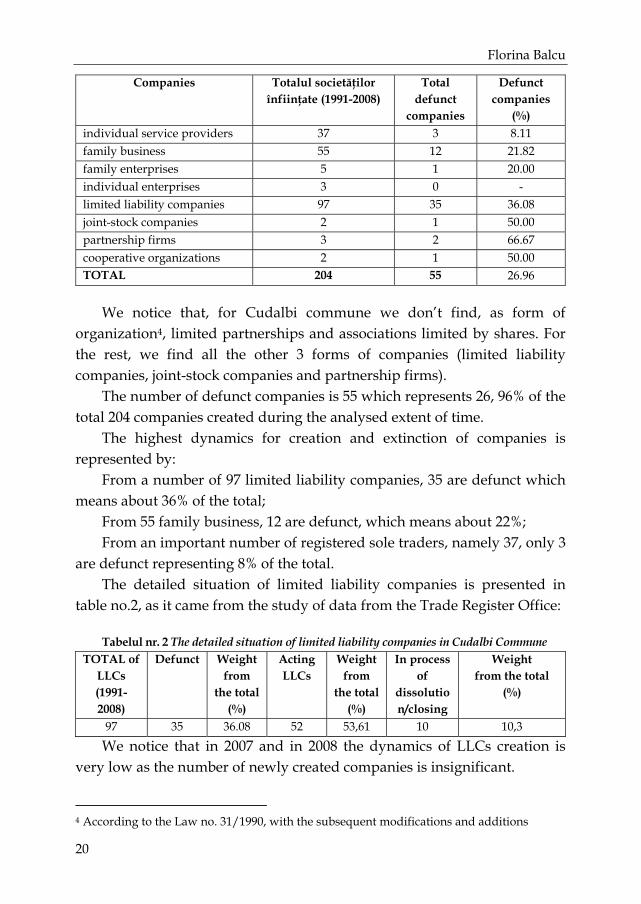

(%) individual service providers 37 3 8.11 family business 55 12 21.82 family enterprises 5 1 20.00 individual enterprises 3 0 - limited liability companies 97 35 36.08 joint-stock companies 2 1 50.00 partnership firms 3 2 66.67 cooperative organizations 2 1 50.00 TOTAL 204 55 26.96

We notice that, for Cudalbi commune we don’t find, as form of organization4, limited partnerships and associations limited by shares. For the rest, we find all the other 3 forms of companies (limited liability companies, joint-stock companies and partnership firms).

The number of defunct companies is 55 which represents 26, 96% of the total 204 companies created during the analysed extent of time.

The highest dynamics for creation and extinction of companies is represented by:

From a number of 97 limited liability companies, 35 are defunct which means about 36% of the total;

From 55 family business, 12 are defunct, which means about 22%; From an important number of registered sole traders, namely 37, only 3

are defunct representing 8% of the total. The detailed situation of limited liability companies is presented in

table no.2, as it came from the study of data from the Trade Register Office:

Tabelul nr. 2 The detailed situation of limited liability companies in Cudalbi Commune TOTAL of

LLCs (1991-2008)

Defunct Weight from

the total (%)

Acting LLCs

Weight from

the total (%)

In process of

dissolution/closing

Weight from the total

(%)

97 35 36.08 52 53,61 10 10,3

We notice that in 2007 and in 2008 the dynamics of LLCs creation is very low as the number of newly created companies is insignificant.

4 According to the Law no. 31/1990, with the subsequent modifications and additions

Evaluative Study for Cudalbi Commune, Galati Department

21

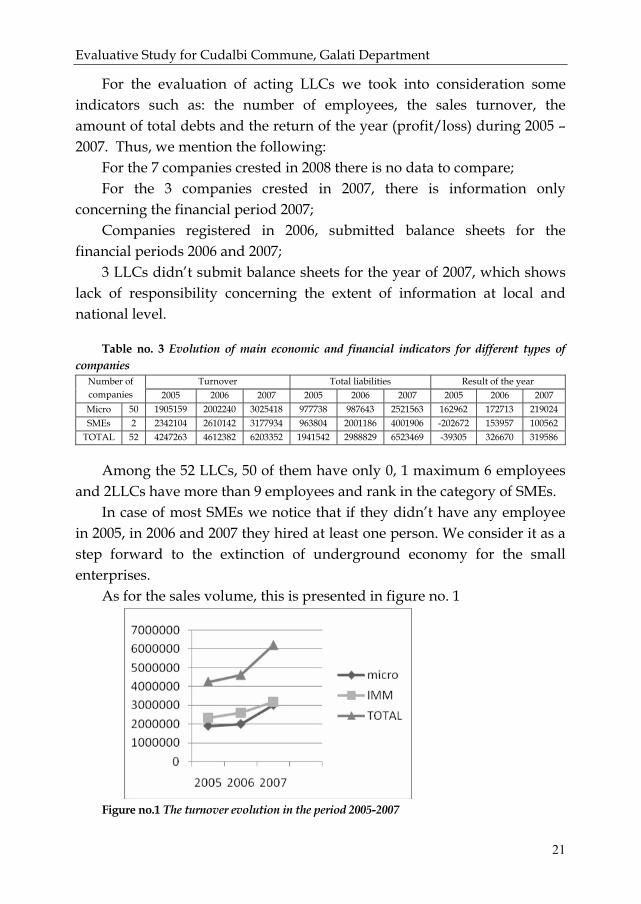

For the evaluation of acting LLCs we took into consideration some indicators such as: the number of employees, the sales turnover, the amount of total debts and the return of the year (profit/loss) during 2005 – 2007. Thus, we mention the following:

For the 7 companies crested in 2008 there is no data to compare; For the 3 companies crested in 2007, there is information only

concerning the financial period 2007; Companies registered in 2006, submitted balance sheets for the

financial periods 2006 and 2007; 3 LLCs didn’t submit balance sheets for the year of 2007, which shows

lack of responsibility concerning the extent of information at local and national level.

Table no. 3 Evolution of main economic and financial indicators for different types of companies

Turnover Total liabilities Result of the year Number of companies 2005 2006 2007 2005 2006 2007 2005 2006 2007 Micro 50 1905159 2002240 3025418 977738 987643 2521563 162962 172713 219024 SMEs 2 2342104 2610142 3177934 963804 2001186 4001906 -202672 153957 100562

TOTAL 52 4247263 4612382 6203352 1941542 2988829 6523469 -39305 326670 319586

Among the 52 LLCs, 50 of them have only 0, 1 maximum 6 employees and 2LLCs have more than 9 employees and rank in the category of SMEs.

In case of most SMEs we notice that if they didn’t have any employee in 2005, in 2006 and 2007 they hired at least one person. We consider it as a step forward to the extinction of underground economy for the small enterprises.

As for the sales volume, this is presented in figure no. 1

Figure no.1 The turnover evolution in the period 2005-2007

Florina Balcu

22

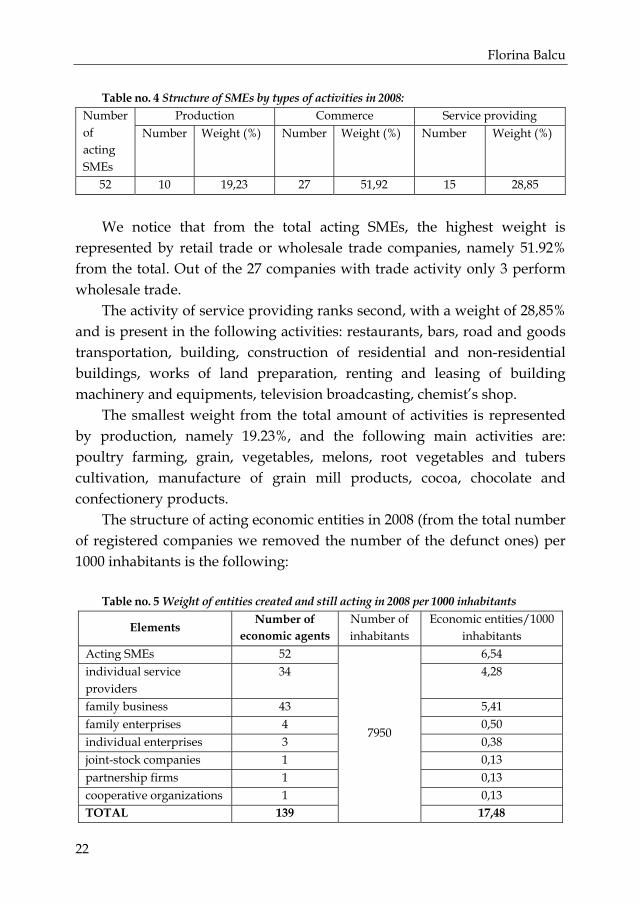

Table no. 4 Structure of SMEs by types of activities in 2008:

Production Commerce Service providing Number of acting SMEs

Number Weight (%) Number Weight (%) Number Weight (%)

52 10 19,23 27 51,92 15 28,85

We notice that from the total acting SMEs, the highest weight is

represented by retail trade or wholesale trade companies, namely 51.92% from the total. Out of the 27 companies with trade activity only 3 perform wholesale trade.

The activity of service providing ranks second, with a weight of 28,85% and is present in the following activities: restaurants, bars, road and goods transportation, building, construction of residential and non-residential buildings, works of land preparation, renting and leasing of building machinery and equipments, television broadcasting, chemist’s shop.

The smallest weight from the total amount of activities is represented by production, namely 19.23%, and the following main activities are: poultry farming, grain, vegetables, melons, root vegetables and tubers cultivation, manufacture of grain mill products, cocoa, chocolate and confectionery products.

The structure of acting economic entities in 2008 (from the total number of registered companies we removed the number of the defunct ones) per 1000 inhabitants is the following:

Table no. 5 Weight of entities created and still acting in 2008 per 1000 inhabitants

Elements Number of

economic agents Number of inhabitants

Economic entities/1000 inhabitants

Acting SMEs 52 6,54 individual service providers

34 4,28

family business 43 5,41 family enterprises 4 0,50 individual enterprises 3 0,38 joint-stock companies 1 0,13 partnership firms 1 0,13 cooperative organizations 1 0,13 TOTAL 139

7950

17,48

Evaluative Study for Cudalbi Commune, Galati Department

23

The number of acting SMEs reported in 2008 per 1000 inhabitants5 is 6, 54, which represents a value well below the national average and below the South-East region value (14,8/1000). For comparison, we mention that the value of SME indicator per thousand inhabitants in the European Union is 52/thousand inhabitants. Given that these are acting SMEs established in the commune, therefore local private initiative, we consider that their small number suggest the need to stimulate initiative among small entrepreneurs.

Even in terms of all private economic entities of the commune, the indicator stands at 17.48 / thousand inhabitants, a figure which we believe it is good to be exceeded for short and medium term in order to increase the number of private entrepreneurs.

Increasing the number of SMEs at national and local level will be possible only provided that the Romanian business environment becomes more predictable, and the structural funds will become more accessible, in a direct and non-bureaucratic way.

On the second place after the initiative of creation of SMEs, is the creation of family business, which shows a preference to work in a personal environment that provides security and prosperity for the family business, and on the third place we find individual service providers that carry on various individual activities, especially retail.

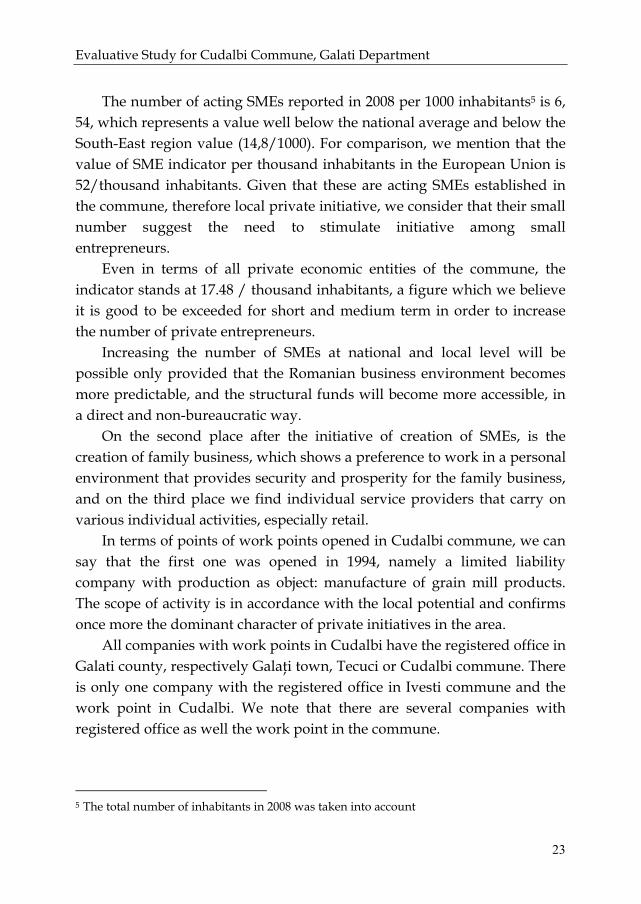

In terms of points of work points opened in Cudalbi commune, we can say that the first one was opened in 1994, namely a limited liability company with production as object: manufacture of grain mill products. The scope of activity is in accordance with the local potential and confirms once more the dominant character of private initiatives in the area.

All companies with work points in Cudalbi have the registered office in Galati county, respectively Galaţi town, Tecuci or Cudalbi commune. There is only one company with the registered office in Ivesti commune and the work point in Cudalbi. We note that there are several companies with registered office as well the work point in the commune.

5 The total number of inhabitants in 2008 was taken into account

Florina Balcu

24

There is no company with the registered office outside the county and work points in Cudalbi commune.

Table no. 4 The situation of work points in Cudalbi during 1994 – 2008

Foundation year

Head office Pincipal activities Total point of work

1994-1999

2000-2008

Galaţi Tecuci Cudalbi Iveşti production commerce Service providing

56 8 48 27 10 18 1 8 40 8

We notice that before 2000 only 8 work points were set up, the most active dynamics is after this year, this stage corresponding to a general dynamic at national economic level, to the opening of borders and to EU adhesion, to changes in law and taxation.

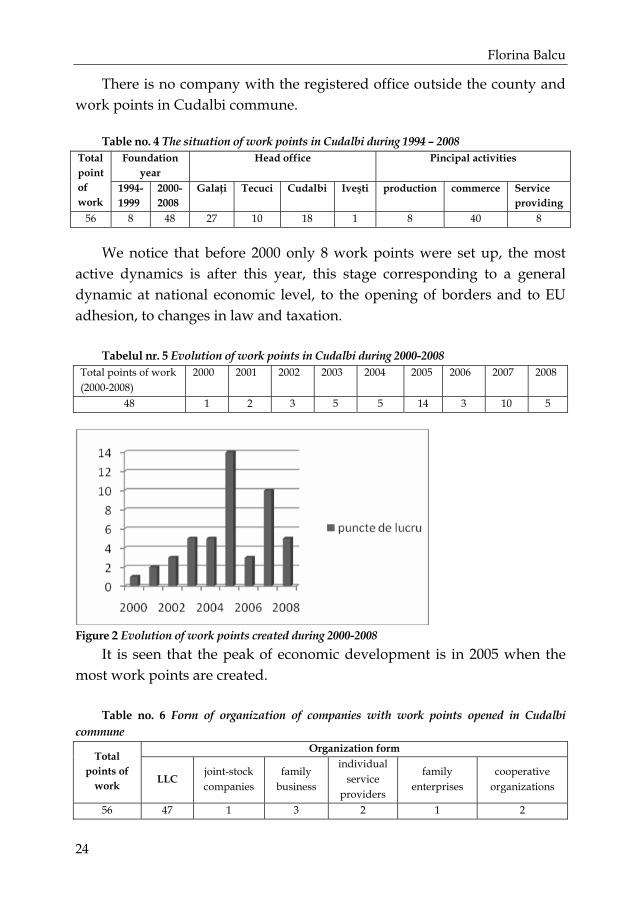

Tabelul nr. 5 Evolution of work points in Cudalbi during 2000-2008 Total points of work (2000-2008)

2000 2001 2002 2003 2004 2005 2006 2007 2008

48 1 2 3 5 5 14 3 10 5

Figure 2 Evolution of work points created during 2000-2008

It is seen that the peak of economic development is in 2005 when the most work points are created.

Table no. 6 Form of organization of companies with work points opened in Cudalbi commune

Organization form Total

points of work

LLC joint-stock companies

family business

individual service

providers

family enterprises

cooperative organizations

56 47 1 3 2 1 2

Evaluative Study for Cudalbi Commune, Galati Department

25

The predominant form of organization of entities with opened work points is limited liability company (LLC).

Only one joint-stock company has a warehouse for grain storage as a work point, opened in February 2008, for a period of 10 years, according to the loan contract completed and submitted to the Trade Registry Office.

The types of activities are production, commerce and services providing. The production activities refer to:

- Manufacture of grain mill products; - Manufacture of bread and fresh pastry; - Manufacture of metal wire products; - Oil production; - Poultry husbandry; - Dairy cattle husbandry; - Vegetables, melons, root vegetables and tubers cultivation. - Activities within the scope of trade refer mostly to retail carried

on in stores such as: - Retail in unspecialized stores predominantly selling food,

beverages and tobacco; - Retail sale of beverages in specialized stores - Retail sale of household articles and appliances, of radios and

TV sets - Retail sale of furniture, lighting articles and other household

products, but also, - Stands and market retail.

There are also two work points carrying on wholesale trade, established in 2007, respectively:

- Wholesale trade of other non-food consumer goods and - Wholesale trade of timber and building material. - The activity of service providing through the 8 work points is

represented by services in the area: - Restaurants, bars and other activities of serving drinks; - Activities of telecommunications through cable networks; - Activities of play and bets - Other leisure and fun activities.

There is only one banking work point since 1998, namely a credit cooperative.

Florina Balcu

26

The existence of work points of entities with main activities in Galati and Tecuci also entails investment from their part which contributed to the economic development of the area and implicitly the creation of jobs.

The partial conclusion leads to the aim concerning the stimulation of private activity at the level of Cudalbi commune by means of adopting some measures to stimulate the investors as well as the inhabitants to create small business.

3. Conclusions

The economic evolutions are based on the dynamics of the main indicators of the economic activity in the commune, on the correlations between them, adding to them the economic results registered at national level. The main economic activities that the commune can certainly rely on and is going to develop are: agriculture, trade, and small-scale agricultural food production and handicraft wares. But these don’t exclude other economic activities which could depend on external circumstances and decisions.

The strategic aim for Cudalbi commune is to provide a dynamic and stimulating local business environment to increase the gross local product.

The recommended possible actions, as a result of the activity carried on by the project team are:

- Investment in infrastructure as precondition of attractiveness to potential investors and local initiatives;

- Investment planning and design in line with internal and external (national and local) funding opportunities.

The economic situation at present for Cudalbi commune is centred upon the agricultural sector, the number of SMEs is quite small per thousand inhabitants and there is a quite low attraction for companies outside the village. Actions that should be covered are related to the supporting of local initiatives for organic farming and processing, exploitation of unused assets and the growth of gross local product by increasing the capacity of the economic agents in the commune. Increasing revenue in the local budget would be a justified action under the circumstances.

Forecasts can focus on two likely scenarios: optimistic and pessimistic.

Evaluative Study for Cudalbi Commune, Galati Department

27

The pessimistic scenario has in view: - Unstable macroeconomic framework generated by current

economic context at national and global extent; - economic policies, especially fiscal, changeable policies; - waste of resources (human, natural, financial); - keeping of the underground economy; - low accumulation rate; - marginalization of the commune within the county

development policy; - Declining revenue and reduction of revenue to the local budget - Low budget expenditure.

The optimistic scenario for the social-economic development is based on several assumptions:

- the favourable macroeconomic and legal framework; - the attraction of some investors from the county or from the

region; - improvement of business environment; - development of entrepreneurship ; - the attractive investment climate of the commune; - the efficient public-private cooperation; - Improvement of management capacity.

Forecasts for future long-term costs integrate the idea that the volume of budgetary expenditure will be based on community capacity to respond to its initiated requests.

Bibliography:

Boloş Ioan Marcel, Bugetul şi contabilitatea comunităţilor locale între starea actuală şi posibilităţile de modernizare, Editura Economică, Bucureşti, 2006

Iftimoaie Cristian, Vedinaş Verginia, Sandu Teodora Gabriela, Urziceanu Carmen, Administraţia publică locală în România în perspectiva integrării europene, Ed. Economică, Bucureşti, 2003

Zaiţ Dumitru, Spalanzani Alain, Cercetarea în economie şi management. Repere epistemologice şi metodologice, Ed. Economică, Bucureşti, 2006

*** Studiul Bugetele locale între teorie şi practică realizat de Institutul Pentru Politici Publice (IPP) la comanda Asociaţiei Pro Democraţia în cadrul proiectului Administrare eficientă prin participare publică finanţat de German Marshall Fund of The United States, 2001

Florina Balcu

28

http://modernizare.mai.gov.ro/ http://www.mie.ro/ http://www.administratie.ro/ http://www.ziare.com

*** Legea nr. 31 din 16/11/1990 privind societăţile comerciale, republicată în Monitorul Oficial, Partea I,nr. 1066 din 17 noiembrie 2004, inclusiv modificările şi completările aduse de următoarele acte: Legea nr. 302/2005, Legea nr. 164/2006, Legea nr. 441/2006, Legea nr. 516/2006, O.U.G. nr. 82/2007, O.U.G. nr. 52/2008 publicată în MOF nr. 333 din 30/04/2008.

Ordonanţă de urgenţă nr. 44 din 16/04/2008 Publicat in Monitorul Oficial, Partea I nr. 328 din 25/04/2008 privind desfăşurarea activităţilor economice de către persoanele fizice autorizate, întreprinderile individuale şi întreprinderile familiale

Legea nr. 273/2006 privind finanţele publice locale, pubicată în Monitorul Oficial nr. 618 din 18 iulie 2006, care abrogă Ordonanţa Guvernului nr. 45 din 2003.

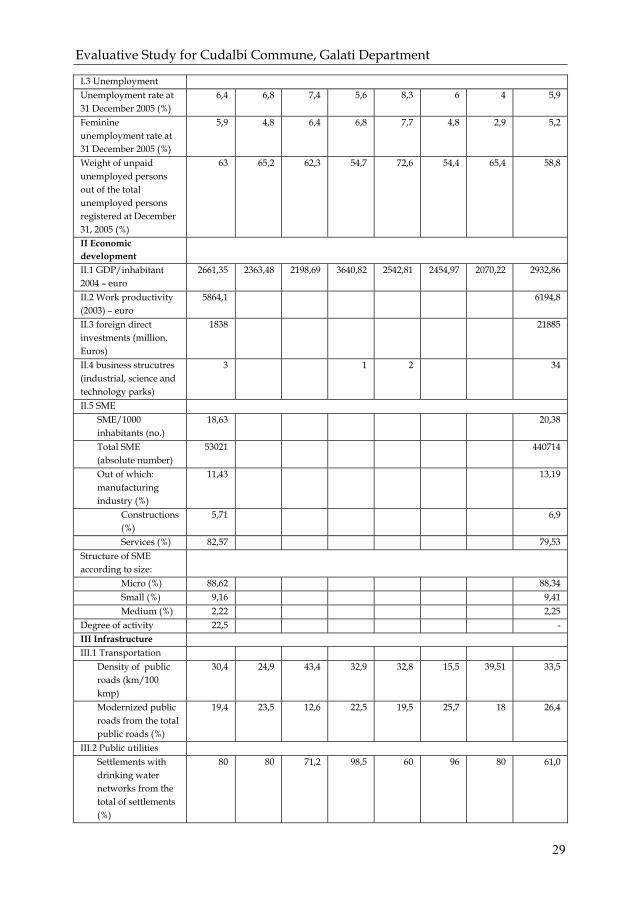

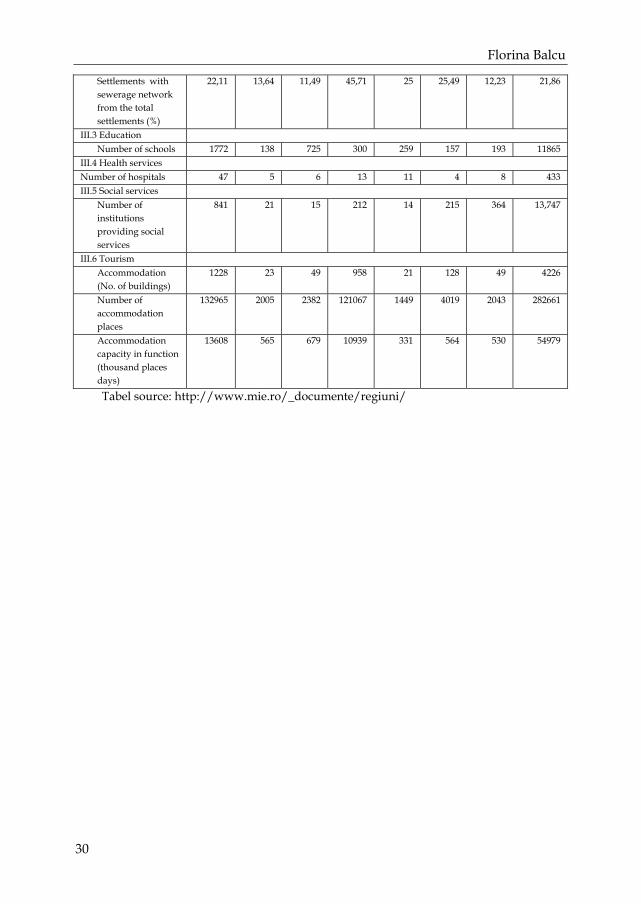

Appendix 1 Indicators that characterize the level of development and the economic potential of the South-East Region (2006):

COUNTIES6 INDICATORS Region BR BZ CT GL TL VN

Romania

I Population, employment, unemployment

I.1 total population (absolute numbers)

2846379 370428 494052 715148 620500 252485 393766 21623849

Urban population (%)

55,5 65,3 41,4 70,9 56,9 49,1 37,8 54,9

Rural population (%)

44,5 34,7 58,6 29,1 43,1 50,9 62,2 45,1

Migratory balance -1803 -499 -379 675 -1095 -590 -142 -7234 I.2 Employment

Active population from the total population (%)

43,7 45,5

Employed population from the total population (%)

36,1 34 36,5 40,1 33,0 34,7 36,2 38,8

Employed population on economic sectors

Agriculture (%)

35,3 33,8 44,9 24,5 31,9 40,0 48,4 32

Industry (%) 21,5 27,5 22,4 17,8 23,3 23,2 19,5 23,5 Services (%) 43,2 38,7 32,7 57,7 44,8 36,8 32,1 44,5

6 The counties included in the South-East region are: Brăila (BR), Buzău (BZ), Constanţa (CT), Galaţi (GL), Tulcea (TL) şi Vrancea (VN)

Evaluative Study for Cudalbi Commune, Galati Department

29

I.3 Unemployment Unemployment rate at 31 December 2005 (%)

6,4 6,8 7,4 5,6 8,3 6 4 5,9

Feminine unemployment rate at 31 December 2005 (%)

5,9 4,8 6,4 6,8 7,7 4,8 2,9 5,2

Weight of unpaid unemployed persons out of the total unemployed persons registered at December 31, 2005 (%)

63 65,2 62,3 54,7 72,6 54,4 65,4 58,8

II Economic development

II.1 GDP/inhabitant 2004 – euro

2661,35 2363,48 2198,69 3640,82 2542,81 2454,97 2070,22 2932,86

II.2 Work productivity (2003) – euro

5864,1 6194,8

II.3 foreign direct investments (million. Euros)

1838 21885

II.4 business strucutres (industrial, science and technology parks)

3 1 2 34

II.5 SME SME/1000 inhabitants (no.)

18,63 20,38

Total SME (absolute number)

53021 440714

Out of which: manufacturing industry (%)

11,43 13,19

Constructions (%)

5,71 6,9

Services (%) 82,57 79,53 Structure of SME according to size:

Micro (%) 88,62 88,34 Small (%) 9,16 9,41 Medium (%) 2,22 2,25

Degree of activity 22,5 - III Infrastructure III.1 Transportation

Density of public roads (km/100 kmp)

30,4 24,9 43,4 32,9 32,8 15,5 39,51 33,5

Modernized public roads from the total public roads (%)

19,4 23,5 12,6 22,5 19,5 25,7 18 26,4

III.2 Public utilities Settlements with drinking water networks from the total of settlements (%)

80 80 71,2 98,5 60 96 80 61,0

Florina Balcu

30

Settlements with sewerage network from the total settlements (%)

22,11 13,64 11,49 45,71 25 25,49 12,23 21,86

III.3 Education Number of schools 1772 138 725 300 259 157 193 11865

III.4 Health services Number of hospitals 47 5 6 13 11 4 8 433 III.5 Social services

Number of institutions providing social services

841 21 15 212 14 215 364 13,747

III.6 Tourism Accommodation (No. of buildings)

1228 23 49 958 21 128 49 4226

Number of accommodation places

132965 2005 2382 121067 1449 4019 2043 282661

Accommodation capacity in function (thousand places days)

13608 565 679 10939 331 564 530 54979

Tabel source: http://www.mie.ro/_documente/regiuni/

31

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor din România

„Contabilitatea a devenit, odată cu globalizarea economiilor, o veritabilă armă economică”

Delesalle F.-E.

Florina Balcu*

Rezumat: În contextul actual, comunicarea rezultatelor devine un exerciţiu de stil aparte.

Rapoartele anuale s-au îmbunătăţit din punct de vedere cantitativ şi calitativ, iar politica asupra prezentării rezultatului constituie o axă centrală a comunicării şi un pol de excelenţă (de perfecţiune). Mai mult decât modul de întocmire, de comunicare şi de prezentare a rezultatelor contează natura şi calitatea reală a evenimentului prezentat. Pot fi influenţaţi utilizatorii de informaţii prin politica de comunicare a rezultatelor? Putem avea o încredere oarbă în comunicarea financiară?

Cuvinte cheie: globalizare, grupuri de societăţi, informaţie contabilă

1. Introducere

Apariţia grupurilor de societăţi şi amploarea procesului globalizării a determinat importante mutaţii ce au avut loc pe plan economic, juridic, social, fiscal, şi, nu în ultimul rând, contabil.

Prezenţa mai multor entităţi juridice în cadrul aceluiaşi grup, antrenează existenţa atâtor contabilităţi independente câte societăţi există. Documentele contabile şi financiare ale fiecărei societăţi în parte nu pot furniza o imagine globală asupra grupului.

În numeroase situaţii societatea-mamă este de tip holding, care nu exercită nici o activitate industrială sau comercială. Bilanţul acesteia este constituit în marea lui majoritate fie din imobilizări financiare (sub forma * Facultatea de Ştiinte Economice, adresa: str. Nicolae Bălcescu 59-61, Galaţi, e-mail: [email protected]

Florina Balcu

32

titlurilor de participare care permit exercitarea unui control sau a unei influenţe asupra altor societăţi), fie din împrumuturi acordate întreprinderilor din grup.

Conturile societăţii-mamă vor apare în acest caz numai ca un mijloc de reflectare a participaţiilor înregistrate sau al dividendelor pe care ea le primeşte sau pe care le-a înscris în contul de profit şi pierdere.

Aici intervine necesitatea consolidării şi a întocmirii situaţiilor financiare consolidate la nivelul grupurilor de societăţi.

Structura de grup oferă întreprinderilor avantaje considerabile în raport cu alte structuri. Profesorul Jacques Richard, de la Universitatea Paris Dauphine identifică o serie de avantaje printre care1:

- structura de grup permite societăţii-mamă un control asupra unui capital mai mare decât cel investit de ea;

- structura de grup facilitează accesul la împrumuturi mai mari; - se realizează o mai bună circulaţie a capitalurilor; - prin structura sa, grupul plăteşte, în general, mai puţine

impozite; - structura de grup oferă posibilităţi mai bune de organizare.

Am putea afirma că două dintre avantajele grupurilor par a avea o importanţă cu totul specială: supleţea şi controlul.

Supleţea se probează în cadrul operaţiilor financiare de restructurare a activităţilor. Diferenţierea acestora în sânul unor entităţi juridice distincte permite o definire mai clară a responsabilităţilor, micşorându-se riscurile la nivelul grupului, atunci când una dintre filiale traversează o perioadă de dificultăţi economice şi financiare. În acest context, operaţiile de cesiune sau de schimburi de acţiuni sunt mai simple şi mai puţin costisitoare decât vânzările diferitelor componente ale activului.

Aplicarea regulilor majorităţii în luarea deciziilor permite să se exercite puterea în mod plenar, fără să se deţină totalitatea acţiunilor. Crearea de filiale şi subfiliale conduce în aceste situaţii la o de multiplicare a puterii în raport cu capitalul efectiv deţinut.

Activitatea societăţilor multinaţionale a generat pe plan contabil, o insuficienţă a informaţiile oferite de contabilitatea financiară, determinând

1 Richard Jaques, Analyse financiere et gestion des groupes, Editura Economica, Paris, 2000, p. 10-16

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor...

33

astfel apariţia unei “noi contabilităţi”, contabilitatea consolidată, ce are drept obiectiv o cât mai bună informare a utilizatorilor prin intermediul situaţiilor financiare consolidate.

În acest context, consolidarea conturilor apare ca obiectiv primar, iar întocmirea şi interpretarea situaţiilor financiare consolidate ca o consecinţă şi un deziderat în vederea unei gestionări cât mai bune a grupului, precum şi a diferitelor categorii de interese din cadrul acestuia.

Consolidarea este o tehnică sau un procedeu ce permite realizarea conturilor unice pentru un ansamblu de societăţi independente, cu personalitate juridică, şi care depind din punct de vedere financiar de un centru de decizie comun. Ea permite prezentarea situaţiilor financiare, a bilanţului contabil şi a rezultatului ansamblului de societăţi ca şi când ar fi al unei singure entităţi.

Obiectivul consolidării conturilor „este de a furniza o imagine fidelă asupra patrimoniului şi situaţiei financiare în ceea ce priveşte rezultatul ansamblului consolidat constituit din întreprinderile cuprinse în perimetrul de consolidare”.2

Scopul consolidării conturilor este „de a prezenta rezultatul operaţiunilor şi situaţia financiară a societăţii-mamă şi a filialelor sale, ca şi când grupul ar fi o singură societate cu mai multe sucursale sau diviziuni”.3

Rezultatul procesului de consolidare îl reprezintă conturile consolidate. Scopul acestora este prezentarea situaţiei şi poziţiei financiare, precum şi a rezultatelor entităţilor cuprinse în perimetrul de consolidare ca şi cum ar fi vorba de o singură întreprindere. Am putea afirma astfel despre conturile consolidate că reprezintă documentele financiare de sinteză ale unui grup, întocmite şi prezentate ca şi cum ar fi întocmite de o singură entitate economică.

Conturile consolidate au o istorie destul de recentă, primele fiind publicate la sfârşitul secolului al XIX-lea, în Statele Unite ale Americii.

Textele de referinţă privind conturile consolidate sunt concretizate în: - Directiva a VII-a a Comunităţilor Economice Europene 83/349/EEC

din data de 13 iunie 1983 privind conturile consolidate, publicată în

2 Bărbăcioru Victoria, Iacob Constanţa, Contabilitate aprofundată, Editura Sitech, Craiova, 1996, p. 117 3 Capron Michel, Contabilitatea în perspectivă, traducere, Editura Humanitas, Bucureşti, 1994, p. 61

Florina Balcu

34

Monitorul Oficial al Uniunii Europene nr. L 193 din data de 18 iulie 1983, cu modificările şi completările ulterioare;

- IAS 27 „Situaţiile financiare consolidate şi contabilizarea participaţiilor în societăţile controlate”, modificat în 2008 sub denumirea de „Situaţii financiare consolidate şi individuale”;

- IAS 28 „Contabilizarea participaţiilor în întreprinderile asociate”; - IAS 31 „Informarea financiară relativă la participaţiile în

întreprinderile de tip joint-venture”; - IAS 21 „Efectele variaţiilor de curs ale monedelor străine”; - IFRS 3 „Combinări de întreprinderi” care, începând din 2005,

înlocuieşte vechiul standard IAS 22, cu aceeaşi denumire şi următoarele interpretări:

SIC 9 Grupări de întreprinderi – Clasificarea în achiziţii şi uniuni de interese

SIC 22 Grupări de întreprinderi – Ajustări ulterioare ale valorii juste şi fondului comercial iniţial raportate

SIC 28 Grupări de întreprinderi – Data schimbului şi valoarea justă a instrumentelor de capital

IFRS 3 a fost modificat de IFRS 5 Active imobilizate deţinute pentru vânzare şi activităţi întrerupte, care a fost publicat în martie 2004. De asemenea, în ianuarie 2008, IASB a emis un IFRS 3 revizuit. Următoarele interpretări se referă la IFRS 3:

SIC 32 Imobilizări necorporale – Costuri asociate creării de website-uri (publicat în martie 2002 şi modificat de IFRS 3 în martie 2004);

IFRIC 9 Reevaluarea instrumentelor derivate încorporate (publicat în martie 2006)

În ţara noastră, cadrul juridic de organizare şi funcţionare a grupurilor de societăţi îl reprezintă Ordinul nr. 3055 din 2009 cu aplicabilitate de la 1 ianuarie 2010 care abrogă Ordinul nr. 1.752 din 17 noiembrie 2005 pentru aprobarea reglementărilor contabile conforme cu directivele europene, emis de Ministerul Finanţelor Publice şi publicat în Monitorul Oficial nr. 1.080 din 30 noiembrie 2005, care abrogă totodată vechiul Ordin al Ministerului Finanţelor nr. 772/2000 de aprobare a Normelor privind consolidarea conturilor.

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor...

35

În conformitate cu aceste norme, grupul este un ansamblu de societăţi, format din societatea care consolidează (persoana juridică română) şi filialele acesteia, societăţi române şi străine (consolidate).

Ca şi în cazul situaţiilor financiare întocmite de agenţii economici, şi la nivelul grupului se poate vorbi de existenţa unor utilizatori interni şi externi ai informaţiilor furnizate de conturile consolidate. Beneficiarii activităţii de consolidare pot fi enumeraţi astfel a fi, în principal, formaţi din:

conducerea întreprinderii mamă – ce are drept scop utilizarea conturilor consolidate drept izvor de date pentru luarea deciziilor în ceea ce priveşte întreprinderile din cadrul perimetrului;

acţionarii grupului de întreprinderi – doresc o mai bună cunoaştere a modului în care le sunt gestionate resursele financiare investite, precum şi interesele lor patrimoniale;

viitorii investitori – care vor putea face astfel evaluări privind viitorul grupului;

angajaţii şi oricine mai doreşte să cunoască situaţia reală a grupului; statul – în nevoia sa de a-şi exercita prin intermediul organismelor

specifice activitatea de control şi aspecte legate de fiscalitate.

2. Studiu asupra situaţiei actuale de comunicare a informaţiilor la nivelul grupurilor de societăţi din România

Analizând stadiul actual al legislaţiei privind consolidarea conturilor putem desprinde următoarele concluzii: în exerciţiul financiar 1 ianuarie 2005 – 31 decembrie 2005, grupurile de societăţi româneşti nu au avut obligaţia redactării de situaţii financiare consolidate, fiind abrogate condiţiile impuse de Ordinul Ministrului Finanţelor publice nr. 772 din 2000. Normele ce constituie obiectul acestui ordin rămân în vigoare şi pot fi totuşi utilizate pentru consolidare de către grupurile care, pentru necesităţi interne de gestiune sau la cerea anumitor utilizatori, doresc să întocmească situaţii financiare consolidate la data de 31 decembrie 2005.

În noiembrie 2005, ca răspuns la cerinţele Ordinului Ministrului Finanţelor Publice nr. 907/2005 privind aprobarea categoriilor de persoane care aplică reglementări contabile conforme cu Standardele Internaţionale de Raportare financiară, respectiv reglementări contabile conforme cu

Florina Balcu

36

directivele europene, este emis Ordinul Ministrului Finanţelor Publice nr. 1752/2005 pentru aprobarea reglementărilor contabile conforme cu directivele europene. Prin abrogarea ordinului 772/2000, începând cu anul 2006, situaţiile financiare consolidate sunt întocmite în conformitate cu directivele europene conform ordinului 1752/2005, care prevede forma şi conţinutul situaţiilor financiare anuale consolidate, inclusiv regulile de întocmire, aprobare, auditare şi publicare a acestora.

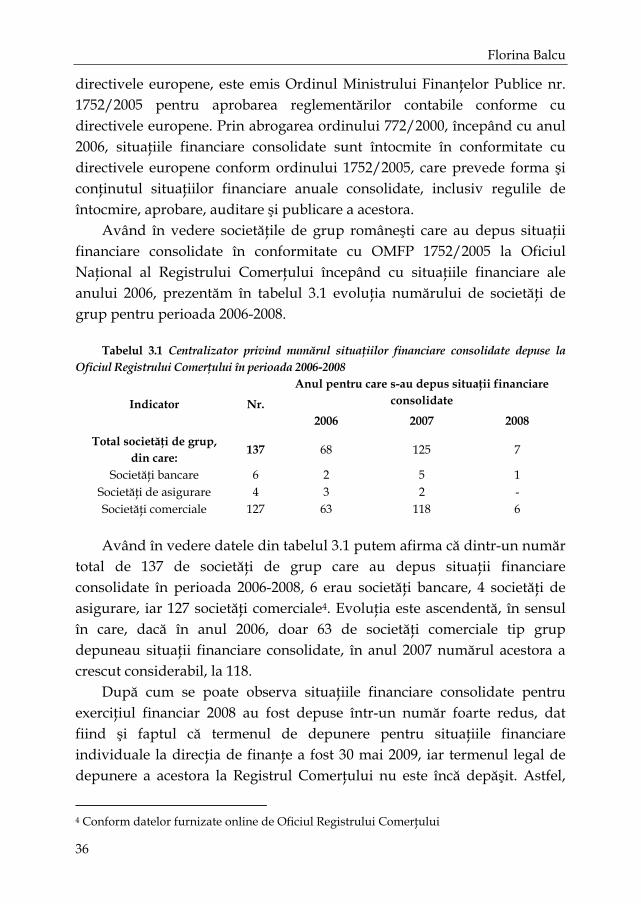

Având în vedere societăţile de grup româneşti care au depus situaţii financiare consolidate în conformitate cu OMFP 1752/2005 la Oficiul Naţional al Registrului Comerţului începând cu situaţiile financiare ale anului 2006, prezentăm în tabelul 3.1 evoluţia numărului de societăţi de grup pentru perioada 2006-2008.

Tabelul 3.1 Centralizator privind numărul situaţiilor financiare consolidate depuse la

Oficiul Registrului Comerţului în perioada 2006-2008 Anul pentru care s-au depus situaţii financiare

consolidate Indicator Nr. 2006 2007 2008

Total societăţi de grup, din care:

137 68 125 7

Societăţi bancare 6 2 5 1 Societăţi de asigurare 4 3 2 - Societăţi comerciale 127 63 118 6

Având în vedere datele din tabelul 3.1 putem afirma că dintr-un număr total de 137 de societăţi de grup care au depus situaţii financiare consolidate în perioada 2006-2008, 6 erau societăţi bancare, 4 societăţi de asigurare, iar 127 societăţi comerciale4. Evoluţia este ascendentă, în sensul în care, dacă în anul 2006, doar 63 de societăţi comerciale tip grup depuneau situaţii financiare consolidate, în anul 2007 numărul acestora a crescut considerabil, la 118.

După cum se poate observa situaţiile financiare consolidate pentru exerciţiul financiar 2008 au fost depuse într-un număr foarte redus, dat fiind şi faptul că termenul de depunere pentru situaţiile financiare individuale la direcţia de finanţe a fost 30 mai 2009, iar termenul legal de depunere a acestora la Registrul Comerţului nu este încă depăşit. Astfel,

4 Conform datelor furnizate online de Oficiul Registrului Comerţului

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor...

37

din totalul de 118 societăţi de grup care au depus situaţii financiare consolidate la 31 decembrie 2007, pânâ la data de 30 mai 2009, doar 6 dintre acestea au depus şi situaţiile aferente pe anul 2008.

Din rândul societăţilor bancare, doar grupul Volksbak Romania SA a depus la Registrul Comerţului situaţiile financiare consolidate şi pentru anul 2008.

Trebuie remarcat, de asemenea, că grupul Flamingo International SA nu apare pe site-ul Oficiului Naţional al Registrului Comerţului ca având situaţiile financiare consolidate depuse la acest organism. Cu toate acestea nu putem menţiona faptul că grupul are situaţiile financiare consolidate postate pe site-ul propriu.

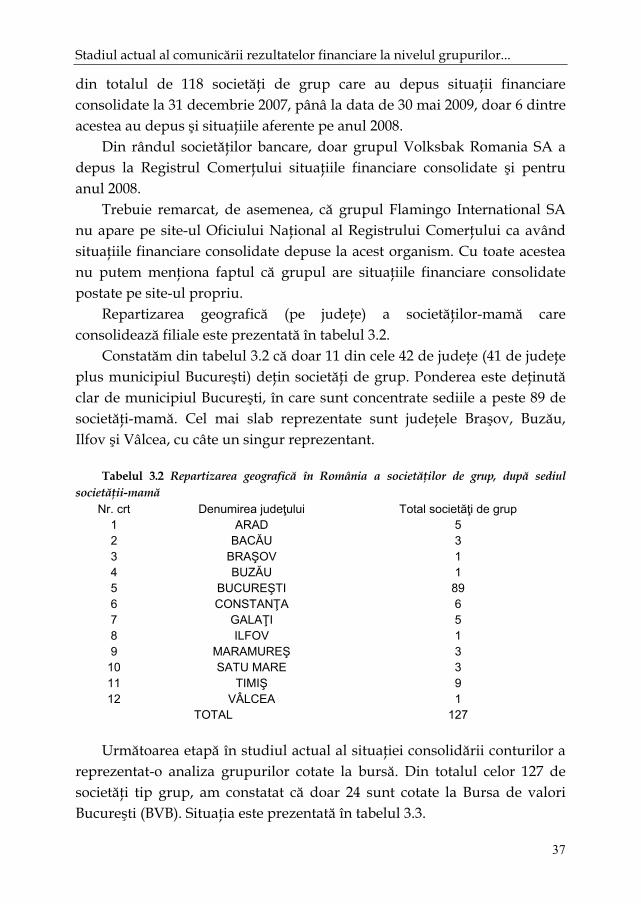

Repartizarea geografică (pe judeţe) a societăţilor-mamă care consolidează filiale este prezentată în tabelul 3.2.

Constatăm din tabelul 3.2 că doar 11 din cele 42 de judeţe (41 de judeţe plus municipiul Bucureşti) deţin societăţi de grup. Ponderea este deţinută clar de municipiul Bucureşti, în care sunt concentrate sediile a peste 89 de societăţi-mamă. Cel mai slab reprezentate sunt judeţele Braşov, Buzău, Ilfov şi Vâlcea, cu câte un singur reprezentant.

Tabelul 3.2 Repartizarea geografică în România a societăţilor de grup, după sediul

societăţii-mamă Nr. crt Denumirea judeţului Total societăţi de grup

1 ARAD 5 2 BACĂU 3 3 BRAŞOV 1 4 BUZĂU 1 5 BUCUREŞTI 89 6 CONSTANŢA 6 7 GALAŢI 5 8 ILFOV 1 9 MARAMUREŞ 3

10 SATU MARE 3 11 TIMIŞ 9 12 VÂLCEA 1

TOTAL 127

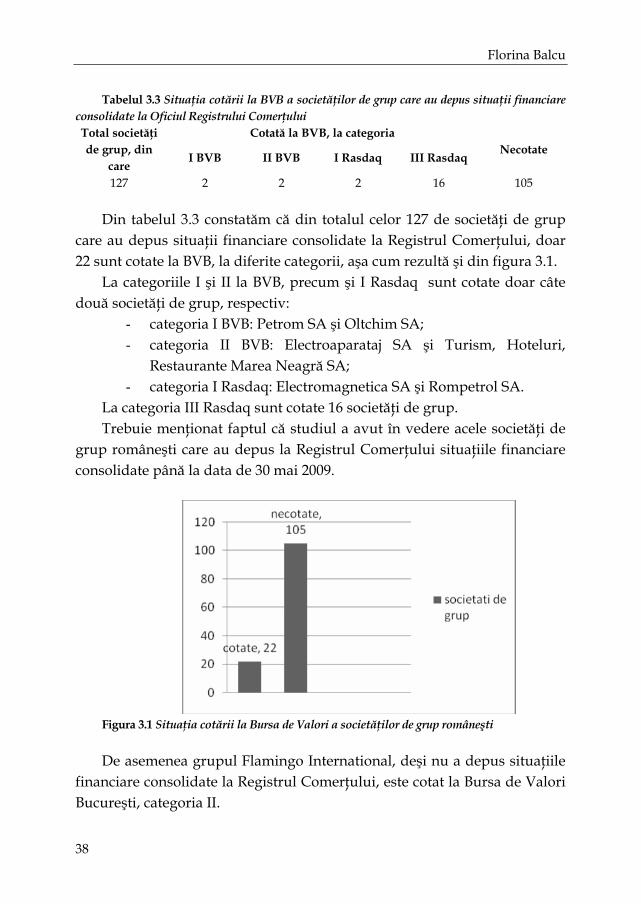

Următoarea etapă în studiul actual al situaţiei consolidării conturilor a reprezentat-o analiza grupurilor cotate la bursă. Din totalul celor 127 de societăţi tip grup, am constatat că doar 24 sunt cotate la Bursa de valori Bucureşti (BVB). Situaţia este prezentată în tabelul 3.3.

Florina Balcu

38

Tabelul 3.3 Situaţia cotării la BVB a societăţilor de grup care au depus situaţii financiare

consolidate la Oficiul Registrului Comerţului Cotată la BVB, la categoria Total societăţi

de grup, din care

I BVB II BVB I Rasdaq III Rasdaq Necotate

127 2 2 2 16 105

Din tabelul 3.3 constatăm că din totalul celor 127 de societăţi de grup care au depus situaţii financiare consolidate la Registrul Comerţului, doar 22 sunt cotate la BVB, la diferite categorii, aşa cum rezultă şi din figura 3.1.

La categoriile I şi II la BVB, precum şi I Rasdaq sunt cotate doar câte două societăţi de grup, respectiv:

- categoria I BVB: Petrom SA şi Oltchim SA; - categoria II BVB: Electroaparataj SA şi Turism, Hoteluri,

Restaurante Marea Neagră SA; - categoria I Rasdaq: Electromagnetica SA şi Rompetrol SA.

La categoria III Rasdaq sunt cotate 16 societăţi de grup. Trebuie menţionat faptul că studiul a avut în vedere acele societăţi de

grup româneşti care au depus la Registrul Comerţului situaţiile financiare consolidate până la data de 30 mai 2009.

Figura 3.1 Situaţia cotării la Bursa de Valori a societăţilor de grup româneşti

De asemenea grupul Flamingo International, deşi nu a depus situaţiile financiare consolidate la Registrul Comerţului, este cotat la Bursa de Valori Bucureşti, categoria II.

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor...

39

Apreciem că opţiunea pentru listarea acţiunilor la bursă, dincolo de necesitatea de a îndeplini şi condiţiile impuse de aceasta, semnifică totodată şi o dorinţă de comunicare a informaţiilor contabil-financiare însoţite totodată şi de transparenţă.

3. Concluzii

Situaţiile financiare consolidate au ca obiectiv reflectarea stării grupului de întreprinderi ca şi cum ar fi o entitate unică, de sine stătătoare, făcându-se abstracţie de personalitatea juridică a fiecăreia dintre filiale. Practic, scopul acestor situaţii este acela de a oferi o reprezentare financiară structurată referitoare la poziţia financiară, performanţele, fluxurile de trezorerie şi tranzacţiile realizate de grup.

Abrogarea, de la 1 ianuarie 2006 a unor importante acte normative care au condus contabilitatea românească până în prezent (OMFP 772/2000, OMFP 94/2001 şi OMFP 306/2002) şi adoptarea OMF nr. 1.752 din 17 noiembrie 2005 pentru aprobarea reglementărilor contabile conforme cu directivele europene, constituie un pas extrem de important pe calea alinierii şi armonizării contabile la nivel internaţional. De asemenea începând cu 1 ianuarie 2010 va intra în vigoare ordinul 3055/2009 care abrogă ordinul 1752/2005 în vederea unei cât mai bune informări şi armonizări.

Elaborarea situaţiilor financiare consolidate se va face, începând cu anul 2006 în conformitate cu normele internaţionale şi, implicit, cu Directiva a VII-a a Comunităţilor Economice Europene. Dacă OMF 772 din 2000 prevedea aplicarea consolidării experimental doar pentru un număr redus de societăţi comerciale, odată cu acest an, situaţiile financiare consolidate reprezintă o cerinţă de întocmire pentru societăţile de grup care îndeplinesc condiţiile legale în vigoare.

Dincolo de conţinutul situaţiilor financiare consolidate prezentate, grupurile sunt încurajate să furnizeze punctele de vedere critice ale conducerii, prin descrierea şi explicarea trăsăturilor principale ale performanţelor financiare, poziţiei financiare, precum şi incertitudinile principale cu care acestea se confruntă. De asemenea grupurile pot să prezinte situaţii adiţionale, precum rapoartele referitoare la mediu şi situaţii privind valoarea adăugată, mai ales în cazul în care activează în

Florina Balcu

40

industrii unde factorii de mediu sunt semnificativi, iar salariaţii reprezintă un grup important de utilizatori. Grupurile de societăţi pot prezenta situaţii adiţionale, în măsura în care factorii de conducere consideră că ele ajută investitorii în luarea deciziilor economice.

În condiţiile globalizării pieţelor financiare pentru grupurile transnaţionale care se finanţează de pe aceste pieţe, alegerea referenţialului contabil care să stea la baza întocmirii şi prezentării situaţiilor financiare consolidate este mai mult decât delicată.

Considerăm căutarea de soluţii comune referitoare la problemele de publicare a conturilor şi a informaţiei financiare demnă de lăudat, în condiţiile în care o abordare unică şi de calitate ar fi cu certitudine mult mai utilă participanţilor de pe pieţele financiare internaţionale, decât mai multe abordări.

Datorită faptului că pieţele internaţionale de capital se integrează, un set unic de standarde internaţionale va spori comparabilitatea informaţiilor financiare şi va face mai eficientă alocarea trans-frontalieră a capitalurilor. În acest mod vor putea fi reduse şi cheltuielile pe care societăţile de grup le suportă în vederea îmbunătăţirii, în acelaşi timp, şi a calităţii auditului.

Adoptarea IFRS în România reprezintă mai mult decât o modificare a reglementărilor contabile. Este un nou sistem de evaluare a performanţei – un nou sistem de proceduri – care trebuie adoptat la nivelul tutror entităţilor economice şi, implicit, la nivelul grupurilor de societăţi.

În concluzie, noile reglementări în domeniu vor schimba modul de lucru şi, de asemenea, este posibil să impună şi schimbări decisive în ceea ce priveşte managementul strategic şi contabil.

Bibliografie:

Albu Nadia, Albu Cătălin, Soluţii practice de eficientizare a activităţilor şi de creştere a performanţei organizaţionale. Gestiunea dezvoltării durabile prin Balanced Scorecard, Ed. CECCAR, Bucureşti, 2005

Balcu Florina, Muntean Mircea, Vîlcu Vasilica, „Reflection on the Importance of the Accounting Information on the Capital Market”, the QIEI 2008 International Conference on Quality – Innovation – European Integration, September 18th-20th, Sibiu, Romania

Balcu Florina, Lupaşc Ioana, Aspects regarding the multinational companies role and direct foreign investments in a globalised economy, al optulea Simpozion

Stadiul actual al comunicării rezultatelor financiare la nivelul grupurilor...

41

Internaţional Investiţiile şi relansarea economică 23-24 mai 2008, ASE Bucureşti, p.82-89, în volumul Investiţiile şi noua economie, Editura ASE Bucureşti, 2008, ISBN 978-606-505-088-4

Bari Ioan, Economia mondială, Editura Economică, Bucureşti, 1997

Bari Ioan, Globalizarea economiei, Editura Economică, Bucureşti, 2005

Bărbăcioru Victoria, Iacob Constanţa, Contabilitate aprofundată, Editura Sitech, Craiova, 1996

Bătrâncea Ioan, Bătrâncea Larissa-Margareta, Bătrâncea Sorin Nicolae Borlea, Analiza financiară a entităţii economice, Editura Risoprint, Cluj-Napoca, 2007

Bătrâncea Ioan, Raportări financiare, Editura Risoprint, Cluj-Napoca, 2006

Bătrâncea, Ioan (coord.), Analiza financiară pe bază de bilanţ, Editura Presa Universitară Clujeană, Cluj-Napoca, 2001

Bătrâncea Maria, Batrancea Larissa, Standing financiar, Editura Risoprint, Cluj-Napoca, 2006

Bech Ulrich, Ce este globalizarea?, Ed. Trei, Bucureşti, 2003

Bunea Ştefan, Optimizarea poziţiei financiare şi a performanţelor întreprinderilor, între strategiile de conservatorism şi de optimism contabil, teză de doctorat, ASE Bucureşti, 2004

Cosma Dorin, Contabilitatea în lumea interdependenţelor globale, Editura Augusta, Timişoara, 1998

Cotleţ Dumitru, Megan Ovidiu, Situaţiile financiare ale întreprinderii, Editura Orizonturi universitare, Timişoara, 2003

Feleagă Niculae, Feleagă Liliana, Contabilitate consolidată. O abordare europeană şi internaţională, Editura Economică, Bucureşti, 2007

Legea nr. 31/1990 privind societăţile comerciale, republicată în Monitorul Oficial nr. 1066/17 noiembrie 2004, cu modificările şi completările ulterioare până la data de 17 aprilie 2009

Legea contabilităţii nr. 82/1991, republicată în Monitorul Oficial, Partea I nr. 454 din 18/06/2008

Legea nr. 297 din 28 iunie 2004 privind Piaţa de capital, publicată în Monitorul Oficial nr. 571 din 29 iunie 2004, cu modificările şi completările ulterioare

Legea nr. 571/2003 privind Codul Fiscal, publicată în Monitorul Oficial nr. 927/2003, cu modificările şi completările ulterioare

Norma nr. 8/2002 privind elaborarea situaţiilor financiare consolidate de către instituţiile de credit publicate în Monitorul Oficial nr. 651/2002

Ordinul Guvernatorului Băncii Naţionale a României nr. 5/2005 pentru aprobarea Reglementărilor contabile conforme cu directivele europene aplicabile instituţiilor de credit.

Ordinul Ministrului Finanţelor Publice nr. 1827/2003 pentru modificarea şi completarea unor reglementări din domeniul contabilităţii

Florina Balcu

42

Ordinul Ministrului Finanţelor Publice nr. 907 din 27 iunie 2005 privind aprobarea categoriilor de persoane juridice care aplică reglementări contabile conforme cu Standardele Internaţionale de Raportare Financiară, respectiv reglementări contabile conforme cu directivele europene

Ordinul Ministrului Finanţelor Publice nr. 1775/2005 pentru aprobarea Reglementărilor contabile conforme cu directivele europene

Ordinul Ministrului Finanţelor Publice nr. 3055/2009 pentru aprobarea Reglementărilor contabile conforme cu directivele europene

43

The ethics of management of the non-reimbursable funds by the romanian SME’s

Diana Bălin*, Aura-Mihaela Ioniţă*

Abstract. The lack of entrepreneurial tradition and education in Romania is

accompanied by severe ethical problems in the Romanian business environment, having consequences at the community level. Taking into account the fact that the SMEs are the direct beneficiaries of the non-reimbursable funds awarded by the European Union in the periods before and after the integration, the management of the input of these funds depends to a great extent on the entrepreneurs’ behaviour as beneficiaries. The cases analysed by the competent institutions (DLAF, DNA) mirror not only procedural errors, but mostly lacks in ethics in the relationship between the private management and the financier. Considering what is involved (loss of sums allotted from the European budget, in case of failed implementations and implicitly a deterioration of Romania’s image as a member state of the EU) we estimate that solving only the already committed cases of fraud is not enough, especially since it is almost impossible to impose an ethical behaviour upon the future beneficiaries. We propose as a solution, complementary to informative actions, the development of preventative actions which will correct the behaviour of the Romanian entrepreneurs in the implementation of financed projects, not only of those who err through ignorance (they do not know), but especially of those who err through ill will (they do not want).)

JEL Classification: A13, D21, F36, L26 Keywords: Ethics, entrepreneurship, European founds, fraud

* Faculty of European Studies. Adress: 1 Em. De Martonne Street, 400090 Cluj-Napoca, Romania. E-mail: [email protected], [email protected] * Faculty of European Studies. Adress: 1 Em. De Martonne Street, 400090 Cluj-Napoca, Romania. E-mail: [email protected]

Diana Bălin, Aura-Mihaela Ioniţă

44

1. Introduction

One of the realities Romania is confronted with as a member of the European Union is the management of the structural funds. This is not all a novelty as during the pre-accession period, the European funds (such as PHARE, SAPARD etc.) have been used for various projects. However, the management of these funds remains a challenge for the public authorities and the SMEs involved, a challenge to integrity and responsibility.